Executive Summary

In 2022, miners faced the perfect storm with a confluence of headwinds that put them in a very precarious position. In the first half of 2023, the storm has begun to pass. The high energy prices that impacted miners in 2022 have subsided as natural gas has retraced significantly, providing miners with variable power relief. Bitcoin price is up 84% coming off the lows of $16,600 from near year-end 2022. Transaction fees have increased three-fold due to the emergence of ordinals, resulting in new demand for blockspace. All these developments have been constructive for Bitcoin miners. But, despite the trend reversal in several key areas of the mining landscape, many of these tailwinds have been offset by the incredible increase in network hashrate during the first half of the year, resulting in record high difficulty. Roughly 121 EH of hashrate was added in the first half of the year driven by improved mining economics, oversupply of ASICs in the secondary market, new generation machines getting plugged in, and broader increases in international hashrate in places like Russia, the Middle East, China and South America. In this report, we delve into each of these major events and trends that have impacted the Bitcoin mining industry in 1H 2023, as well as provide our perspective on the current state of the industry and potential implications of the upcoming halving event.

Key Takeaways

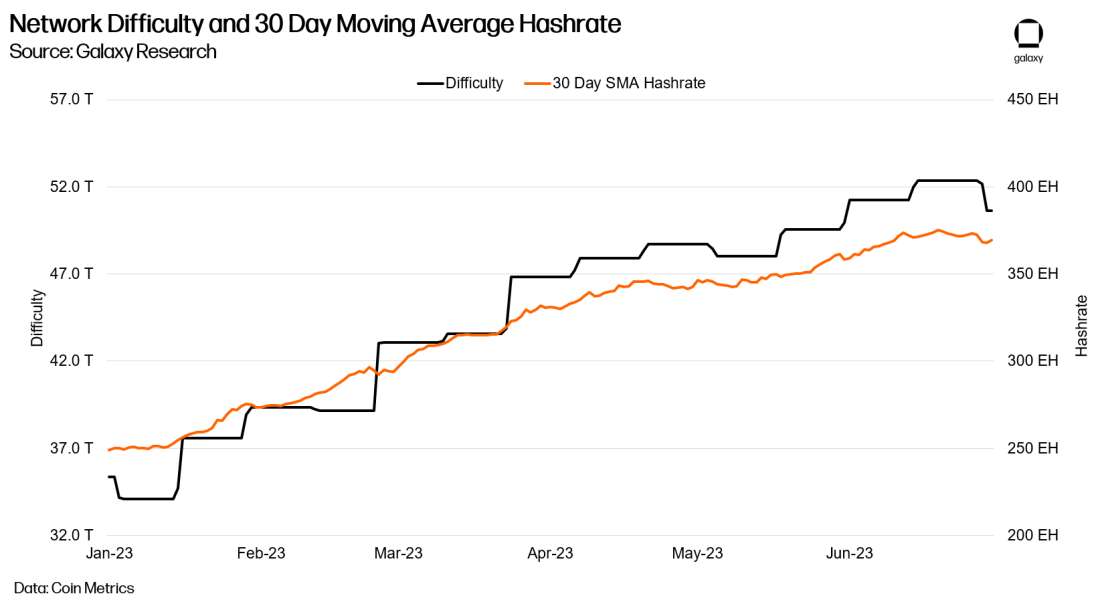

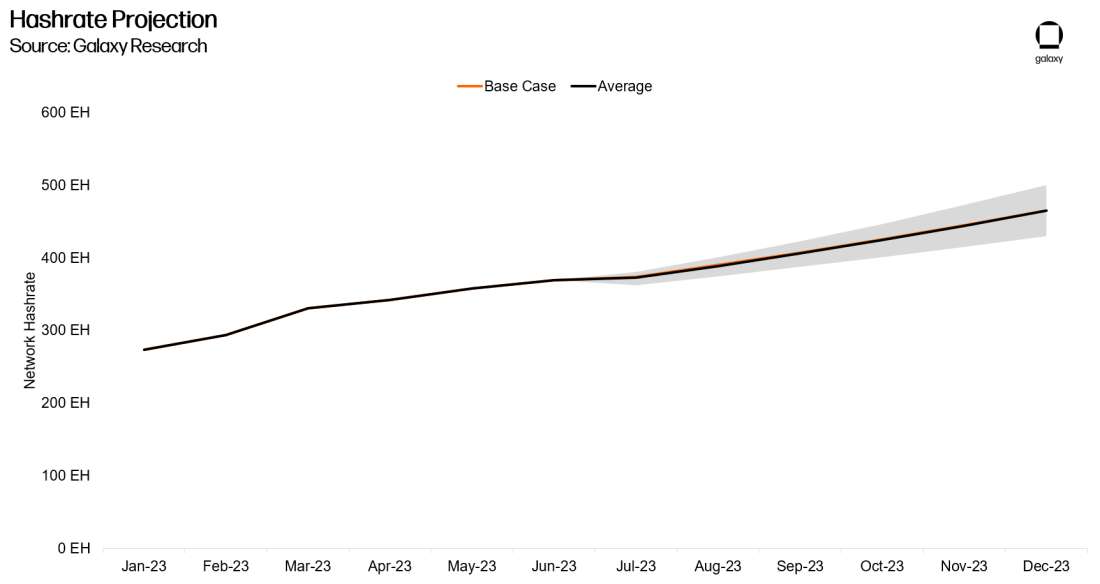

Hashrate and difficulty increases have exceeded expectations with 30D trailing network hashrate increasing 121 EH. Given the availability of ASICs and especially next generation ASICs and our estimated breakeven hashprice for the network being below $0.045 we anticipate a sustained and continued upward trajectory in hashrate through year-end. As result, we have increased our based case end of year hashrate assumption to 465 EH.

Bitcoin’s fourth halving is approaching next year, and miners are actively taking measures to prepare by either pursuing mergers & acquisitions, diversifying their business outside of mining, or upgrading their mining fleet with new generation machines.

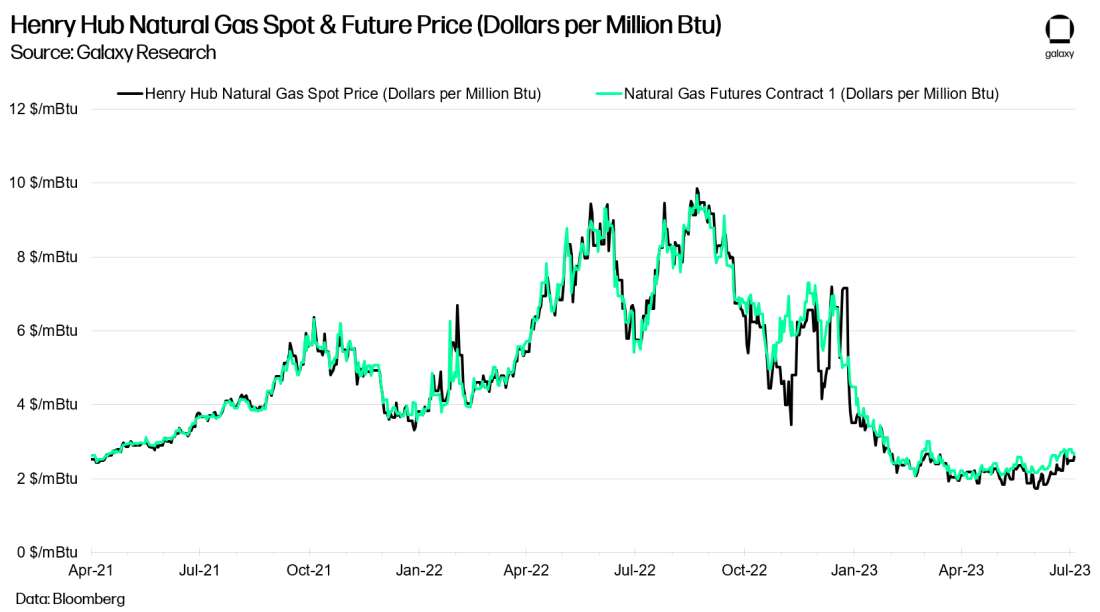

After natural gas increased 145% in 2022 and propelled power prices higher, it has since retraced 72% during the first half of the year, providing a significant tailwind for miners.

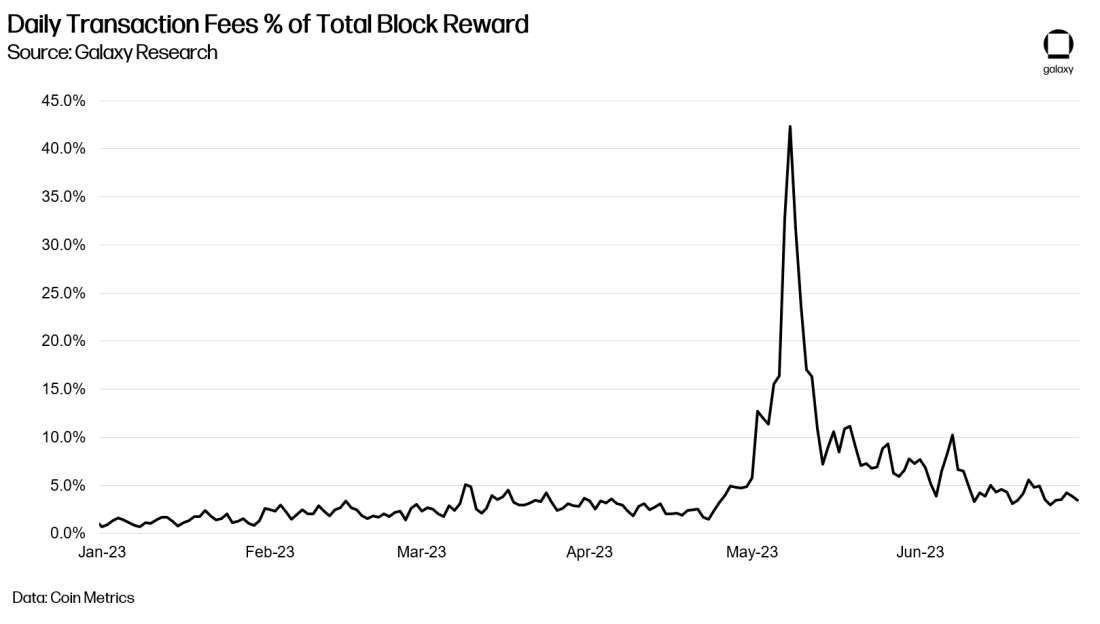

Ordinals have been a complete wild card for miners that has helped to boost transaction fees for the first half of the year, to 8,228 BTC worth $219.8M compared to just 2,324 BTC worth $82.7M during the first half of 2022. This represents a 166% increase YoY in dollar terms and 254% increase in BTC terms.

We expect some degree of hashrate seasonality to emerge again on the network as more miners in ERCOT participate in economic curtailment and 4CP avoidance over the summer months, with some operators potentially being offline over 19% of the time, causing some downward pressure on difficulty.

On the regulatory front, the mining industry continued to see increased hostile activity in 2023 at the both the State and Federal level. Considering the White House becoming increasingly focused on the mining industry over the last year, many regulators at the State level have decided to take action forcing some miners to explore new opportunities outside out the US. Senate Bill 1751 and 1929 also proved that even in what have been deemed as pro-mining jurisdictions such as Texas and the ERCOT grid that mining isn’t completely safe from attack.

Mining Economics

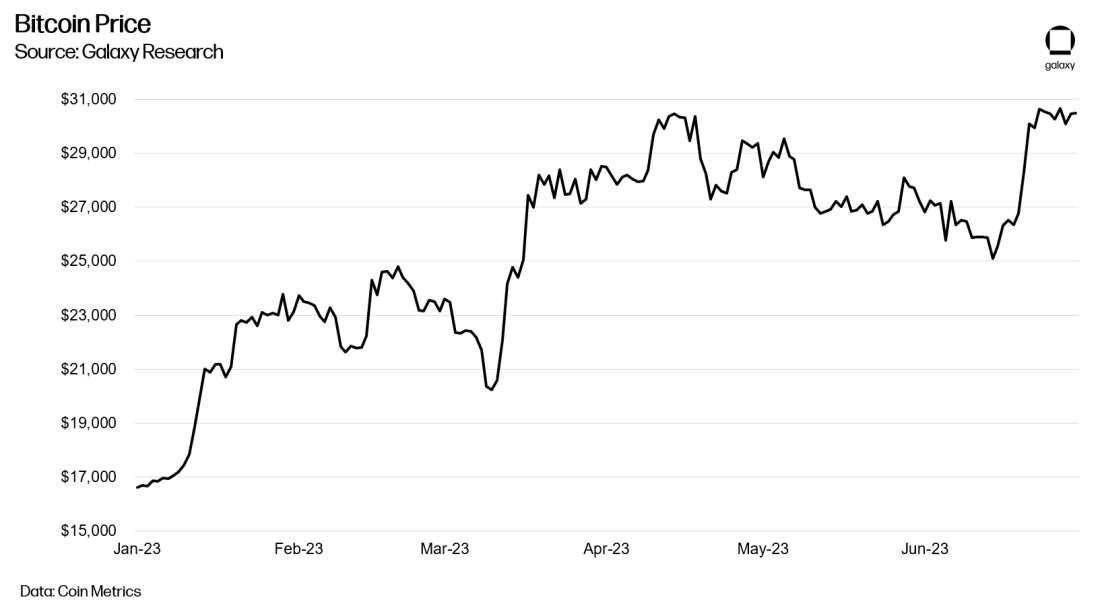

Bitcoin Price Recovery from 2022 Lows

Coming off the near all-time low hashprice levels at the end of 2022, the first half of 2023 has provided miners with some relief despite the tremendous increase in overall network difficulty and hashrate. To start, bitcoin has rallied significantly. From beginning the year at roughly $16,600, bitcoin initially experienced a sharp upward rise in January to $23,000 following an inflation report that suggested the beginning of disinflation. This event instigated a shift in investor sentiment towards risk assets including bitcoin as the market began factoring in a Federal Reserve pivot, resulting in a broader uptick for these assets.

From the end of January to early March, bitcoin price demonstrated remarkable resilience and traded within a $21,000 - $25,000 range before hitting a volatile period when the banking crisis began. However, bitcoin, which was designed precisely to protect against such situations and allows individuals with self-sovereignty over their own funds, managed to thrive. After an initial tumble in price, bitcoin swiftly rebounded to $27,000.

Following this period of turbulence, bitcoin established yet another trading range between $26,000 - $30,000, after which it broke through the key resistance level of $30,000 following news that Blackrock filed with the SEC to launch a spot-based Bitcoin ETF.

Transaction Fee Surge

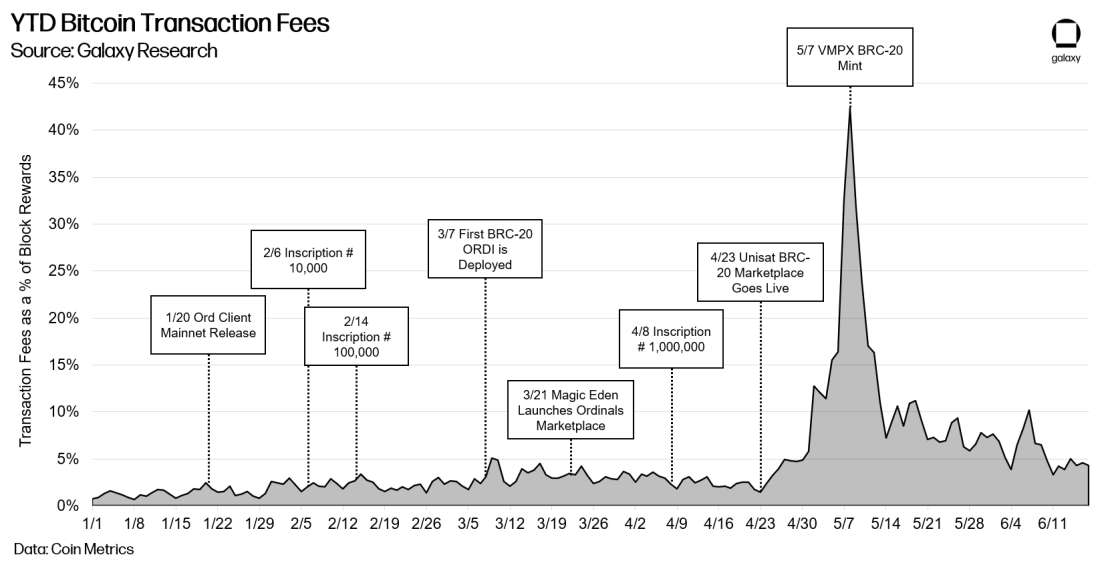

Transaction fees historically have not played a meaningful role in overall miner revenue over a sustained period. In 2022, there was hardly any congestion in the mempool and fees averaged between 1%-3% of total rewards. As we entered 2023, the low fee trend vanished due to the proliferation of inscriptions. Individuals eagerly sought to inscribe satoshis with various forms of art, audio, and text, causing a notable increase in mempool and block sizes. To prevent their transactions from being purged from the mempool and ensure inclusion into blocks, these users attached higher fees to their transactions.

Consequently, fees soared to unprecedented levels as a specific type of inscription, called BRC-20s, grew in popularity. Significant BRC-20 issuance activity drove fees to as high as 50% of total block rewards, or in otherwards, almost equal to the 6.25 BTC block subsidy.

Even after the major spike in fees caused by BRC-20 mania, fees nonetheless remain elevated. Through the course of the first half of 2023, miners accumulated 8,684 bitcoins in total fees, in comparison to the 2,325 bitcoins in fees for the first half of 2022 and the 5,375 bitcoins in total fees amassed throughout the entirety of 2022. This increase in fees demonstrates the substantial financial benefits miners have reaped from the surge in transaction volume and the corresponding rise in fees, as fees go straight to miners’ bottom line. Fees have since come down from their highs as interest surrounding BRC-20s has fallen.

Network Hashrate Grows Relentlessly

Compared to the first half of 2022, network hashrate as grown at a more accelerated pace. From the beginning of 2023, 30D trailing network hashrate has grown 49% from 249 EH to 370 EH compared to a growth rate of 22% in 1H 2022.

While in 2022 much of the hashrate growth could be attributed to the immense amount of capital that flooded the ASIC market in 2021 and machines just getting plugged in, 2023 had its own set of drivers including the growth in bitcoin price, ASIC prices remaining subdued, natural gas prices nosediving, and international miners coming into the picture.

Natural gas prices retraced 72%. The decline in natural gas prices during the first half of the year provided miners with variable rate exposure to power prices with significant relief and thus improved their overall mining margins even with the increases in hashrate.

Bitcoin’s price increased 84%. The increase in bitcoin price helped to also offset much of the hashrate growth that was experienced during the first half of the year.

Transaction fees are up 62% in comparison to total fees for all of 2022. The rise of ordinals significantly increased the demand for blockspace thus causing fees to rise and total block rewards to increase also helping to offset and allow for continued hashrate growth.

The rise of international hashrate. While it is difficult to identify the exact location of where hashrate is coming from we suspect that in the first half of the year regions such as the Middle East, Russia, Latin America, and other parts of the world like Bhutan significantly increased their hashrate exposure.

ASIC Manufacturers continued to produce new generation ASICs at scale. ASIC manufacturers opted to maintain their capacity at foundries and likely have reverted to self-mining with some of those machines as overall demand for new ASICs is down due to the large quantities of supply available on the secondary market stateside.

Miners turned to underclocking machines to improve break-evens. to better weather the storm several miners have been using custom firmware such as LuxOS and Braiins OS+ to underclock S19 series machines and improve their efficiency allowing them to operate profitably at lower breakeven levels.

Hashprice

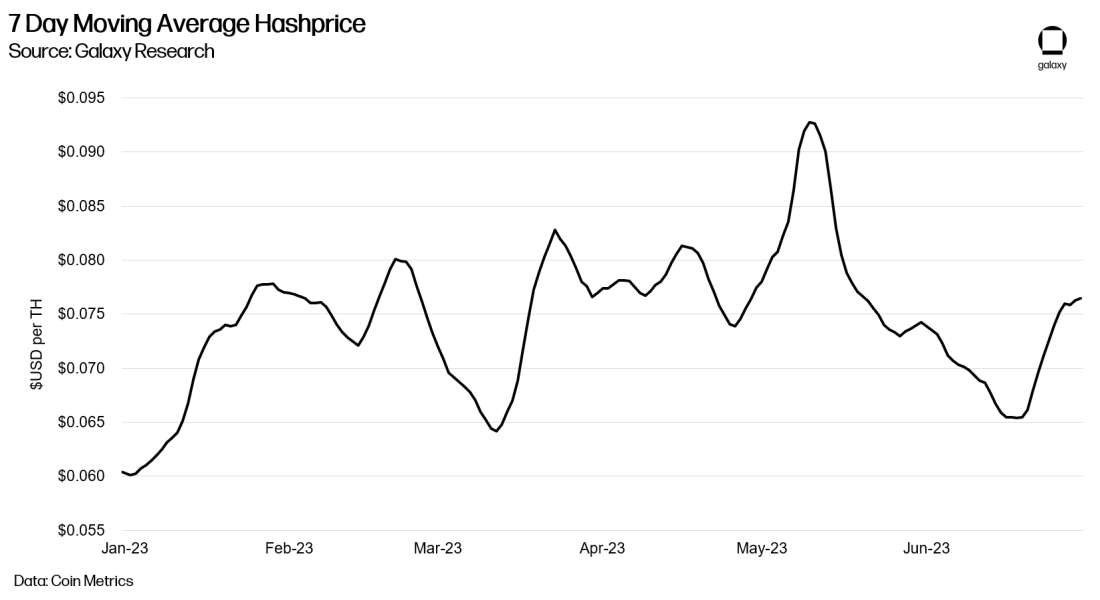

Despite the rise in hashrate, surging bitcoin price and generally higher transaction fees have pushed up hashprice, or the dollar revenue per TH per day. The 7 Day Moving Average Hashprice rose from $0.060/TH to $0.076/TH in the first half of 2023.

Hashrate Forecast

Bitcoin’s 30D moving average network hashrate has increased 49% in the first half 2023 from 249 EH to 370 EH, amounting to 121 EH of additional hashrate. Given that bitcoin’s price at the start of 2023 was $16,600 and hashprice was $0.060, it’s quite shocking how much hashrate has been added in a fairly short period of time. Assuming the average efficiency of machines installed during the first half of the year is equivalent to 27.0 j/TH roughly 3.3 GW of capacity was brought online. There are a few defining events that took place over the course of the first half of the year that have led to this significant hashrate outperformance:

Hashrate Forecast Revision

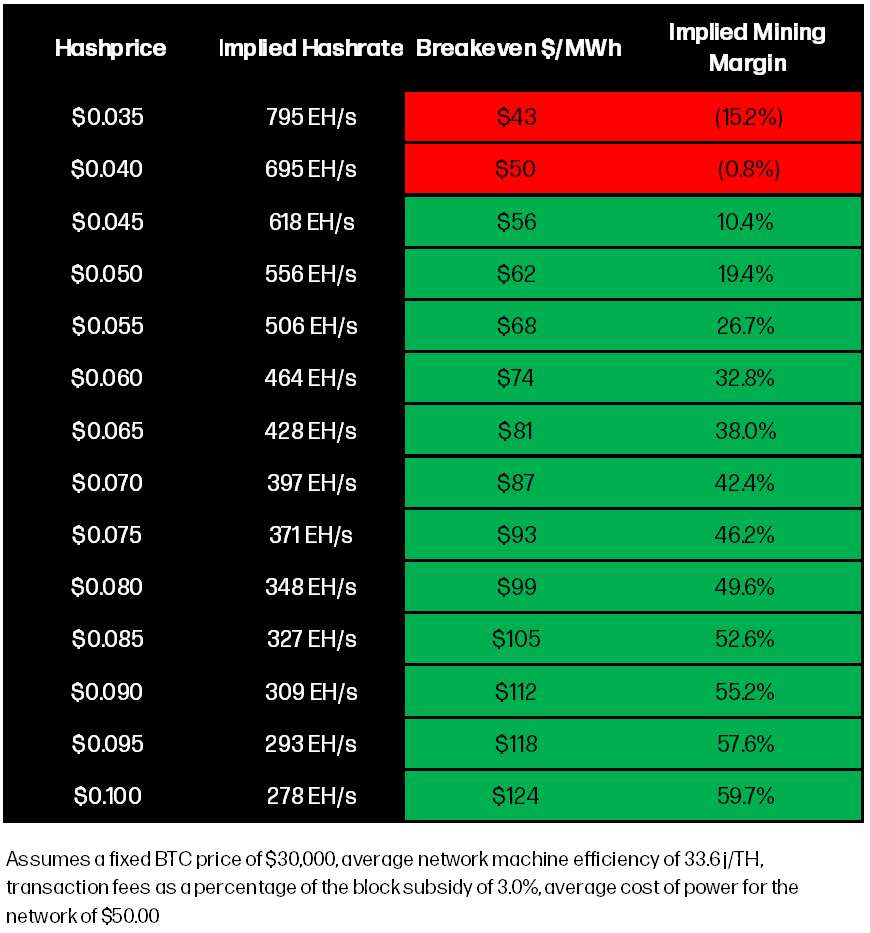

Methodology: We approached our hashrate forecast by trying to understand how much hashrate the network could bear given key assumptions around miners average cost of power, the efficiency of ASICs that make up the network and a fixed bitcoin price assumption. For cost of power, we assume that the average miner’s cost of power is $50 per MWh based on historical energy prices in ERCOT and public miners implied cost of power. For the average efficiency of ASICs in the network we referenced Karim Helmy and Coin Metrics research which uses nonce analysis to estimate average the efficiency to be 33.6 j/TH. Finally, we assume a fixed bitcoin price of $30,000.

With these assumptions, we were able to calculate the total implied amount of network hashrate at various hashprice levels. We can then derive the breakeven $/MWh of the network based on the average machine efficiency of 33.6 j/TH at the various hashprice levels and calculate an implied gross mining margin assuming $50 per MWh cost of power. What is evident from this analysis is that the network could support a significant amount of additional hashrate and that the current breakeven network hashprice is likely around $0.045 or lower. This analysis provides us with a potential theoretical maximum for hashrate. From this starting point, we derived our predictions by considering other factors that are more challenging to quantify but impact the growth of network hashrate such as available capacity, number of ASICs likely available in the market and hashrate targets from public miners.

Bull Case: Ourbull case scenario assumes a trailing 30D end of year network hashrate of 500EH (+101.6% YoY). To hit this target roughly 21.8 EH of hashrate would need to come online per month representing roughly 181,600 ASICs and equating to 545 MW of monthly energization assuming average ASIC efficiency of 25 j/TH predominantly consisting of S19 XP’s and M50 series machines.

Base Case: Ourbase case scenario assumes a tailing 30D end of year network hashrate of 465 EH (+87.5% YoY). To hit this target roughly 16.0 EH of hashrate would need to come online per month representing roughly 133,333 ASICs and equating to 400 MW of monthly energization assuming average ASIC efficiency of 25 j/TH predominantly consisting of S19 XP’s and M50 series machines.

Bear Case: Ourbear case scenario assumes end of year network hashrate of 430 EH (+73.4% YoY). To hit this target roughly 10.2 EH of hashrate would need to come online per month representing roughly 85,000 ASICs and equating to 255 MW of monthly energization assuming average ASIC efficiency of 25 j/TH predominantly consisting of S19 XP’s and M50 series machines.

Themes from 1H 2023

ASIC Market Decorrelation

The ASIC market was significantly impacted by the worsened mining conditions in 2022, resulting in low demand and declining prices. Even though in the first half of 2023 7D average hashprice has increased 27.0% and bitcoin price 84.5% from the start of the year, we’ve seen ASIC prices for popular models such as the S19 series remain flat or even decline. One of the biggest contributing factors to this lack of correlation with bitcoin price is the high amount of machine supply in U.S. secondary markets due to equipment loan defaults, asset sales, and bankruptcies. In 2022, at least 11.59 EH of hashrate collateral that was used for ASIC-backed loans defaulted, leaving lenders with ASICs to either sell or run themselves. In the first half of 2023, there were additional ASIC loan defaults from public miners and an even larger amount of hashrate that was made available in 363 asset sale processes for companies like Core Scientific, Compute North, BlockFi, and Celsius.

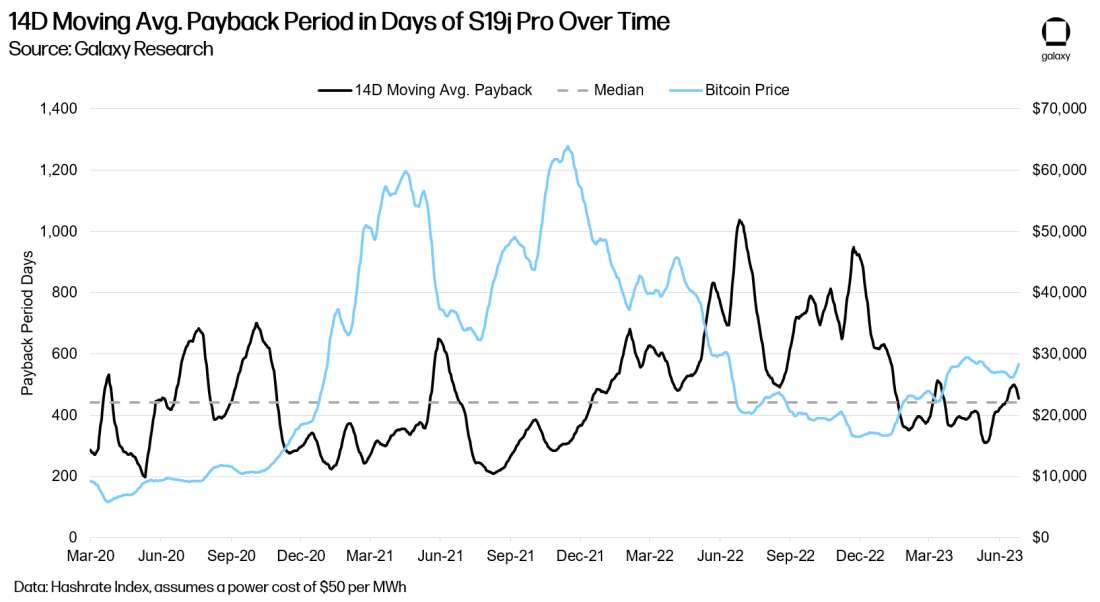

The second biggest contributing factor to ASIC decorrelation is the fact that ASIC manufacturers opted to maintain their capacity at the major foundries. Despite the supply glut that had been growing in the secondary market, Bitmain and MicroBT have continued to ramp up the production of their latest generation of machines, the S19 XP series and the M50 series of machines, respectively. This continuous supply production, when combined with subdued demand, has inhibited ASIC prices. Bitmain is still offering coupons that can be applied against new purchase orders of these machines, keeping prices low in the $16 - $23 per TH range depending on the make and model. This has resulted in a price ceiling for older generation machines such as the S19j Pro even as economics have improved thus improving the implied payback period for these machines.

The third major contributing factor is the looming halving event. The market is pricing in a halving discount for machines, especially for the now older generation machines like the S19j Pro and M30 series. The uncertainty looming around the halving and its ultimate impact on mining economics is causing miners to price in a discount for what they’re willing to pay for machines such that they can ROI on older generation machines with a 10-month payback period or less. This halving discount makes sense, particularly when you take into consideration that market hosting terms currently are in the range of $65 - $75 per MWh assuming no profit share component. Assuming $70 per MWh for power and a hashprice of $0.070 pre-halving, the most a miner should be willing to pay for an M30S is $2.10 per TH and $5.63 per TH for an S19j Pro. Looking ahead, we anticipate that the ASIC market will continue to remain depressed and largely uncorrelated with bitcoin price as we get closer to the halving unless we see a rapid and sustained increase in bitcoin price.

The Rise of Ordinals & Their Impact on Transaction Fees

Ordinals have been one of the most unexpected new frontiers for Bitcoin in 2023 and have had a meaningful impact on transaction fees. Created by Casey Rodarmor, an open-source bitcoin developer, the ORD client runs on top of a Bitcoin Core full node and allows users to encode arbitrary data inside bitcoin transactions and bind that data to an individual Satoshis. The primary use case of this has been on-chain NFTs or digital artifacts but has also paved the way for other ideas such as tokenization with the BRC-20 protocol and DeFi. The popularity of users wanting to create or trade these digital artifacts or tokens has caused significant demand and competition for blockspace. Through the first half of 2023, there have been 14.4M total inscriptions amounting to over $55M of total transaction fees.

We anticipate that ordinals and inscriptions become a buyer of last resort for blockspace and create a sat/vByte floor that should make it difficult for 1 sat/vByte transactions to clear in the mempool. As users continue to experiment with ordinals and different indexing ideas, it is plausible that we will see additional fee spikes and transaction fee volatility, which will benefit miners. For more information on inscriptions and ordinals, read our Galaxy Research report from March.

Energy Prices Cool Down

Disruption in global energy markets in late 2022 and early 2023 due to the conflict in Ukraine resulted in energy commodities, particularly natural gas, to soar in price. Because natural gas is typically the marginal price setter of energy across electrical grids, its movements in price had a major influence over the cost of power for miners and how market hosting rates are determined. In the first half of 2023, natural gas prices came off highs to decline by over 72%, giving relief for miners with floating rate energy exposure.

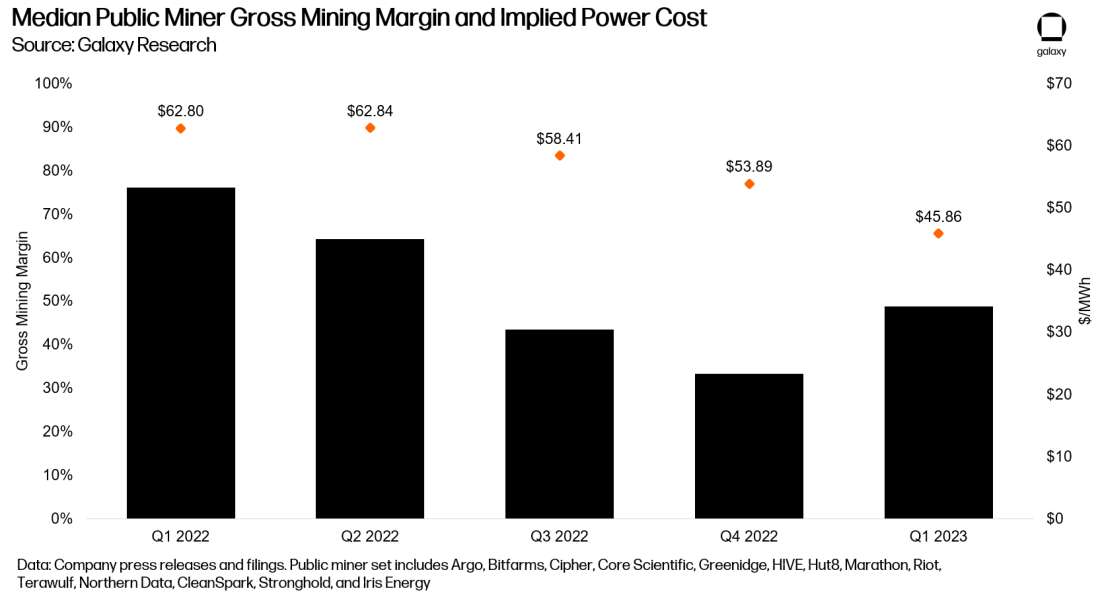

Several shifting market dynamics caused natural gas prices to decline. U.S. dry natural gas production grew, reaching a monthly average record in February 2023 of 101.5 billion cubic feet per day (Bcf/d). By the end of April, U.S. natural gas in storage was 19% above the previous five-year (2018–2022) average at 2,114 billion cubic feet (Bcf). Mild winter temperatures across the U.S. and Europe further reduced demand for natural gas for residential and commercial heating, resulting in less-than-average natural gas withdrawals from storage. Declining energy costs reduced the median power cost for publicly traded bitcoin miners 15% in Q1 2023 from the prior quarter. (We calculate the median power cost by dividing cost of revenue on the income statement by the estimated operational MWhs, itself based on each company’s reported average quarterly hashrate). We anticipate that the Q2 2023 median power cost of publicly traded miners will remain low given that natural gas prices have been flat since the start of Q2 2023. Even though hashrate has remained relatively flat (between $0.065 - $0.075), declining power prices enabled public miners to boost their gross mining margins quite substantially, 16% QoQ from Q4 2022.

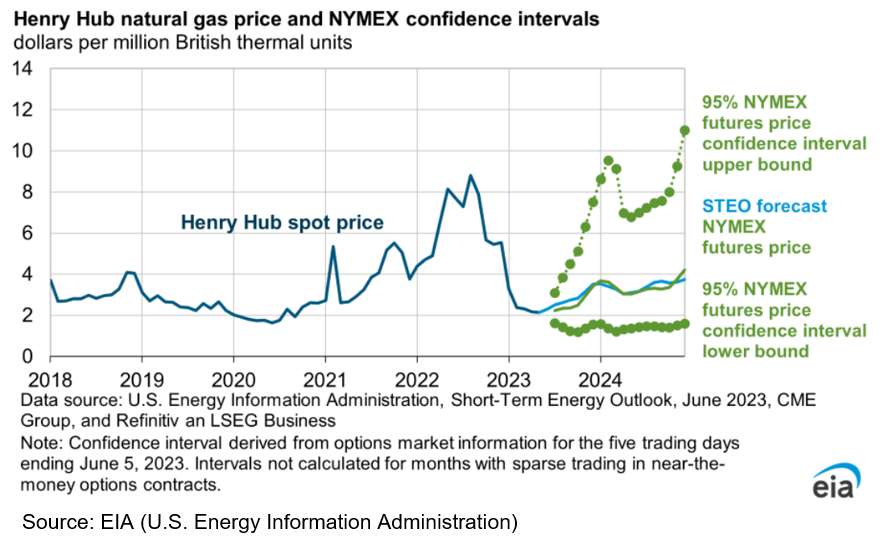

Looking ahead to 2H 2023 regarding natural gas prices, the EIA expects prices to increase throughout the summer as production declines slightly and demand for air conditioning increases the use of natural gas in the electric power sector. The Henry Hub spot price in their forecast averages almost $2.90 per million British thermal units (MMBtu) in 2H23, up from the realized May average of $2.15/MMBtu. The natural gas price at the Henry Hub in our forecast rises by almost 30% in 2024 compared with 2023 to an average of about $3.40/MMBtu.

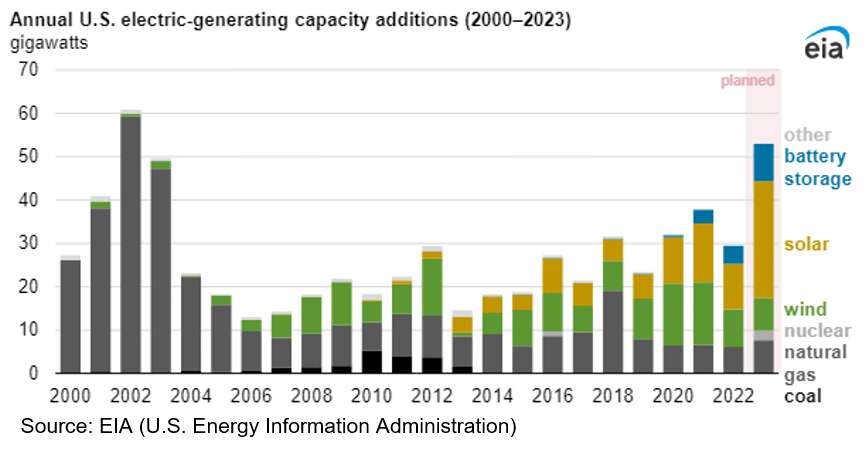

Another major trend in energy to watch is the increase in renewable energy sources and battery capacity being added to the U.S. grids. Wind, solar, and battery storage are increasingly becoming a larger share of net new electric-generating capacity each year. So far in 2023, these three sources of generation accounted for 82% of the new, utility-scale capacity that developers plan to bring online in the United States. Because wind and solar only produce electricity when wind is blowing or the sun is shining, they are intermittent sources of generation. Battery storage helps to mitigate the intermittency issue and serves as a flexible load resource. However, battery storage is very costly, and the overall amount of battery storage being built lags behind the total amount of wind and solar generation coming online.

As a result, there has been a correlation emerging between energy price volatility and the amount of solar and wind coming online in certain areas of the grid. As the supply side or sources of generation on the grid become more inelastic it becomes harder to manage peak demand in a grid leading to more volatility and extremes in energy pricing during these periods. Increased volatility creates more economic curtailment opportunities for miners that have a robust power strategy. More importantly, it is evident that batteries alone cannot bridge the gap for the U.S.’ transition to a more sustainable grid due to capex cost and the availability of raw materials such as cobalt. Miners serve as a market-based, ancillary flexible load resource that can help to balance generation as the grid makes its transition to becoming more sustainable.

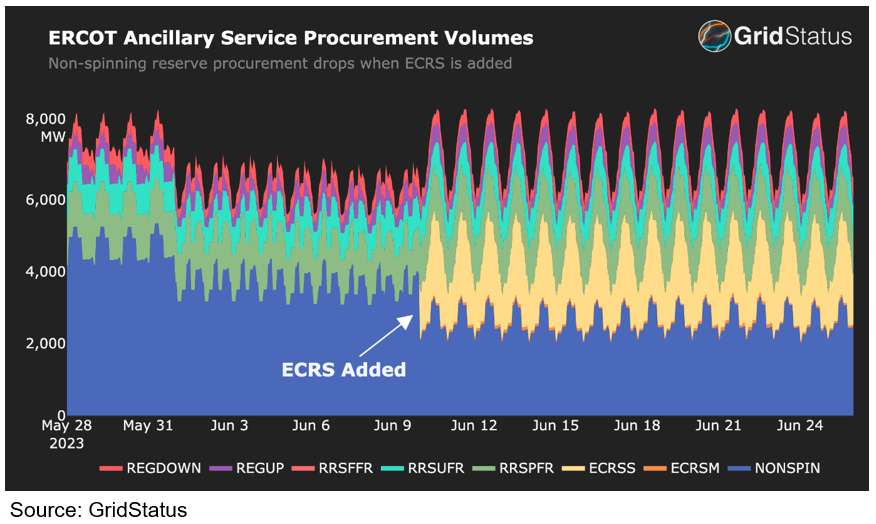

Texas, where a large concentration of U.S. miners is situated presents an instructive example of miners contributing to grid stabilization. On June 10th, ERCOT introduced a new ancillary service for the first time in over a decade: the ERCOT Contingency Reserve Service (ECRS), an ancillary service product designed to address medium-term net load uncertainties, which are increasing due to renewables, and reduce pressure on faster responding ancillary service products, such as frequency regulation.

Ancillary services like frequency regulation were designed to correct for minute-to-minute forecast errors. However, in markets with high solar penetration, everyday occurrences such as sunrise and sunset tend to cause forecasting errors on any given day in only one direction for longer periods of time. Since June 10th, ECRS has contributed a considerable amount of demand response and something we expect to increase as loads such as miners can participate for grid stabilization.

International Miners Driving Hashrate Growth

In 2022, the U.S. led much of the growth in network hashrate and, more specifically, this came from US publicly listed miners. In 2023, however, the relentless growth in hashrate appears to have been driven by miners outside of North America. Although it is difficult to pinpoint the exact location of a miner, the charts below provide an indication of this trend.

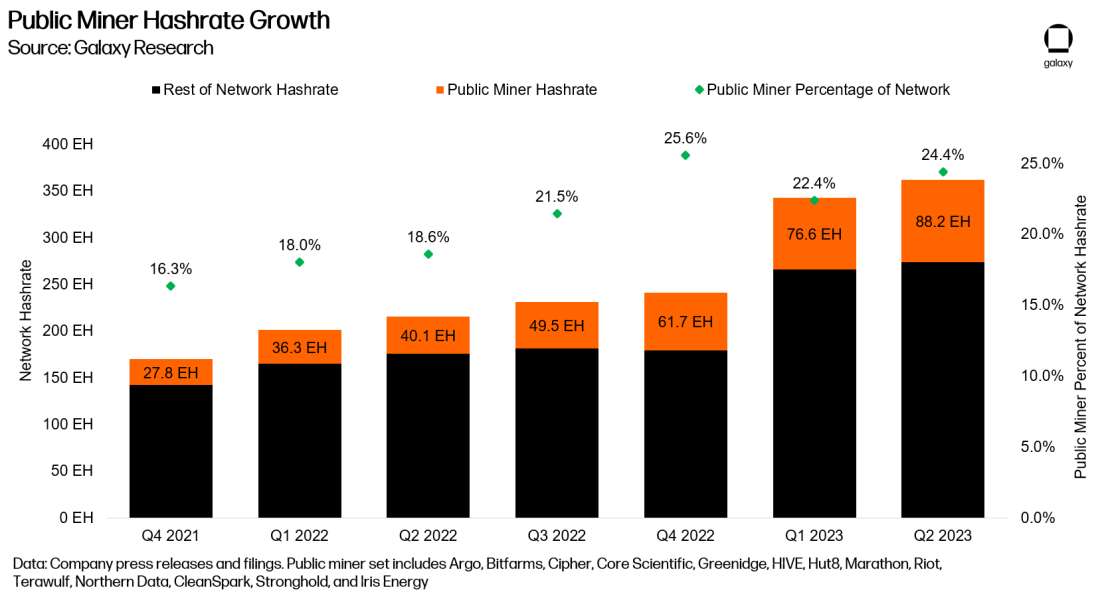

The first chart shows public miners’ hashrate vs. the rest of the network’s hashrate, along with the percentage share of the network that public miners comprised. In 2022, public miners’ hashrate rose from 27.8 EH to 61.7 EH, a 122% increase. This outpaced the growth in network hashrate and resulted in a steady increase in public miners’ share of the overall network from 16.3% at the beginning of 2022 to 25.6% at the end of 2022. Thus, the growth in hashrate was in large part driven by public miner hashrate expansion.

However, as we entered 2023, although public miners have continued to energize machines, the growth in the rest of the network’s hashrate has kept up as well. Public miners’ share of the network has fallen off slightly and plateaued between 22%-25% of the total network hashrate. Since public miners are concentrated predominantly in North America, we believe that larger scale, and potentially state-sponsored, foreign miners have come online during the first half of 2023. While private miners within North America could have also contributed to the growth of the network, we don’t believe that it could have been done at the same scale as international miners, especially if they are state sponsored because of the access to new capital.

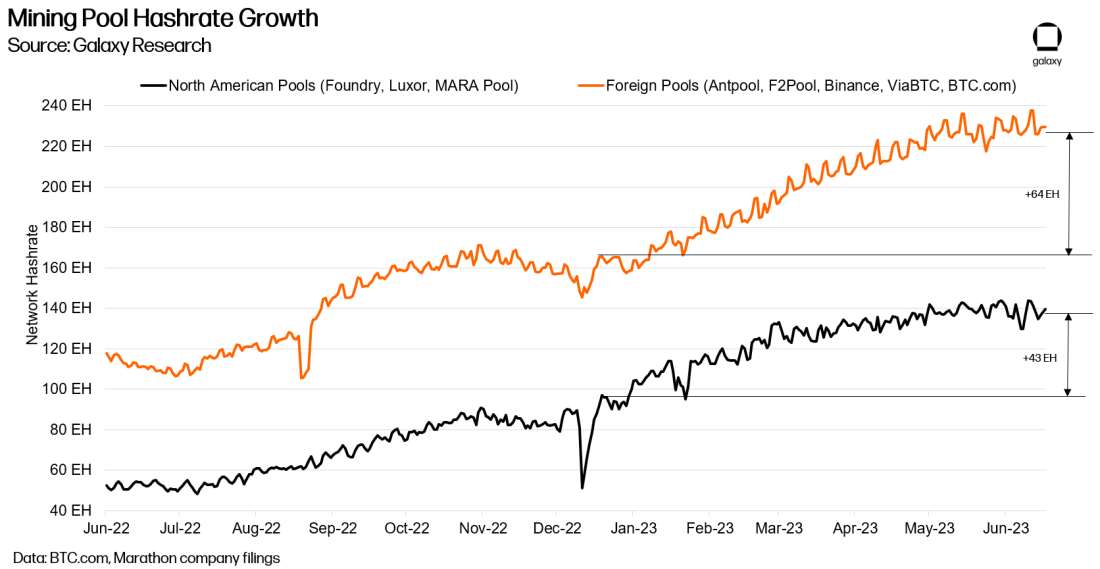

Second, while we caveat that the location of a mining pool operator does not imply miners are also located in that region, we observe that growth in Asia pool hashrate has outpaced growth in North American pool hashrate. Hashrate of pools in Asia rose 64 EH in comparison to North American pools’ 43 EH rise. Asia-based pools cannot pass AML/KYC checks for public miners, who then resort to Foundry, Luxor, or in Marathon’s case, its own pool, MARAPool. We can therefore deduce that growth in Asia-based pools likely comes from other foreign miners. Coupled with the stagnating growth of public miner hashrate relative to the network, this is an indication of overall network hashrate being pushed higher from abroad.

Insights & Trends from Public Miners

Treasury Management & Capital Markets

In the first half of 2023, most miners didn’t deviate much from the treasury management strategies they enacted at the end of last year. Roughly every publicly traded miner has pivoted away from a 100% HODL strategy and nearly every company is either doing some variation of selling all production or enough production to cover operating expenses. Given some of the hard lessons learned during this bear cycle, coupled with the fact that the cost of capital has increased, and debt markets remain closed off, miners will have to ensure that production can cover the cost of electricity, payroll, and other administrative expenses. For these reasons, we anticipate miners to maintain their existing treasury management strategies. However, it is still to be determined for the miners that still maintain a bitcoin treasury whether they will hedge that bitcoin value or look to take profit if price moves to the upside. Failure to properly hedge downside risk of BTC treasuries due to “number go up mentality” last cycle caused miners’ overall liquidity to be reduced by greater than 70% in some cases.

The lack of access to capital markets and the increase in the cost of capital due to the current rate environment has made it difficult for most public miners to be able to expand in a capital efficient manner. Nearly all new growth for public miners is either funded by sales of production in smaller quantities or through dilution from equity ATM programs which comes at a great cost to shareholders. In the first half of the year public miners raised over of $350M from equity sales.

Regulatory Overview

In the United States, regulatory hostility against the bitcoin mining industry continued in 2023 at both the state and federal levels. In direct response to regulatory and policy headwinds of 2022 and 2023, some public miners have announced plans to diversify their operations geographically either through the acquisition of mining sites, JVs or the development of new sites. The perceived hostility to bitcoin mining (and the crypto industry more broadly) in North America has presented an opportunity for other countries with abundant electricity generation to attract miners.

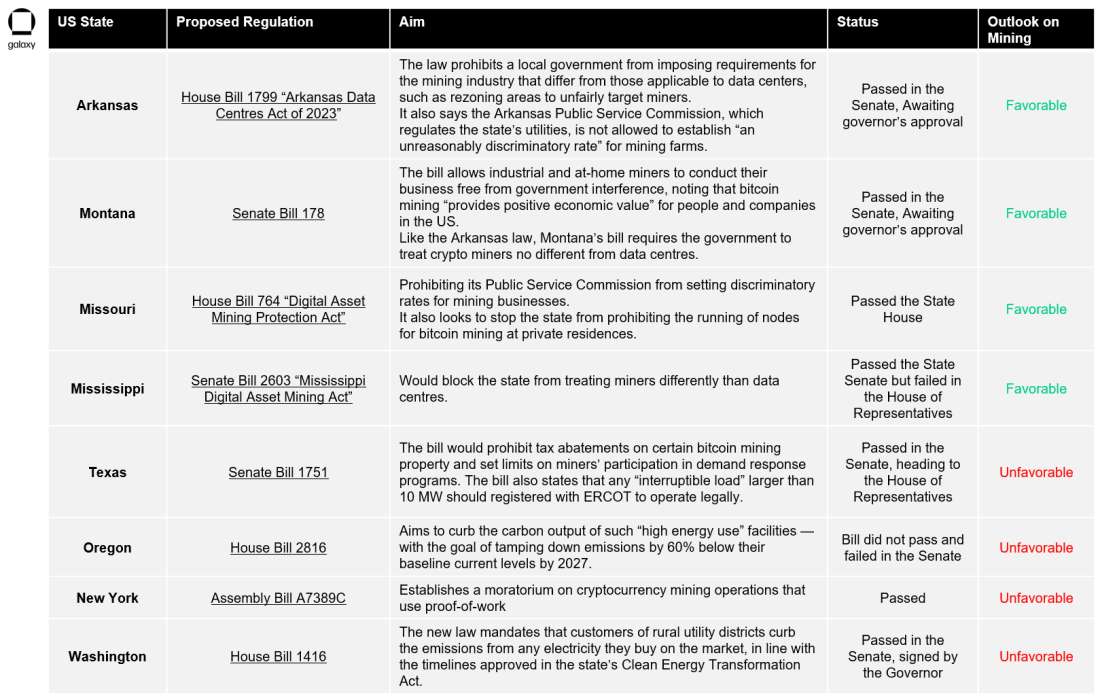

Multiple bills and policies—at a state and federal level—were proposed in the first half of 2023, several of which are detailed below. One of the most surprising developments was the introduction in the Texas state legislature of several bills targeting bitcoin miners in the state, which has been a bedrock jurisdiction for the industry over the last two years. Policies such as these present concrete examples of legislative and regulatory threats to the sector.

Texas Senate Bill 1751:Texas senate proposes Bill 1751 to prevent miners from participating in ancillary services and grid balancing programs

Background and Purpose: The proposed legislation would prohibit tax abatements on certain bitcoin mining property and set limits on miners’ participation in demand response programs. The bill also states that any “interruptible load” larger than 10 MW would be required to register with ERCOT to operate legally.

After unanimously passing the Senate Committee vote, the legislation has been opposed by many Blockchain and Mining non-profit organizations including the Texas Blockchain Council that launched the “Don’t Mess With Texas Innovation” campaign. The campaign received a lot of attention within the crypto community and even the former CEO of ERCOT Brad Jones supported the initiative:

“Bitcoin miners have provided a valuable additional tool for ERCOT’s operators during tight supply conditions: a flexible load that can shut down so that needed electricity can flow to our most vulnerable customers.”

Final action: SB 1751 was passed out of the Senate and sent to the House where it was referred to the Committee on State Affairs. SB 1751 stayed in State Affairs without receiving a hearing or vote.

Texas Senate Bill 1929: Relating to the registration of virtual currency mining facilities in the ERCOT power region that demand a large load of interruptible power.

Background and Purpose: Computing facilities used to mine virtual currencies pose a specific challenge to the electric grid because they can connect to the grid quickly, use large amounts of electricity, and ramp up and down more quickly than traditional industrial loads. To ensure ERCOT can properly manage the electric grid, additional information on the existence of these facilities is needed. Accordingly, Bill 1929 seeks to provide for the registration of virtual currency mining facilities in the ERCOT power region that demand a large load of interruptible power.

Final action: SB 1929 was signed in the House and Senate and has been signed by the Governor as of June 9th. The bill will take into effect on September 1st, 2023.

The DAME (Digital Asset Mining Energy) Tax proposed by the Biden Administration (Federal): Proposing a significant new tax on Bitcoin mining operations.

Background and Purpose: Released as part of Biden’s Budget for 2024, the DAME proposal explicitly states that the tax would be used to “Make Cryptominers Pay for Costs They Impose on Others”. According to the blog post, the tax could raise up to $3.5 billion in revenue over the next 10 years by imposing a tax equivalent to 30% of miners cost of electricity. Miners using clean energy would also be targeted by the bill as the administration stated that:

“The environmental impacts of cryptomining exist even when miners use existing clean power. For example, in the case of communities with hydropower where cryptomining operations are often located, increased electricity consumption by cryptominers reduces the amount of clean power available for other uses, raising prices and increasing overall reliance on dirtier sources of electricity.”

Final Action: U.S. Congressman Warren Davidson (R-OH) confirmed that the tax was removed from the “Fiscal Responsibility Act of 2023” deal between Republicans and Democrats, which raised the national debt ceiling, a win for Bitcoin advocates.

Regulatory Activity is Increasing Across States in the U.S.

As the broader crypto industry becomes a bigger focus for policy makers, some states are beginning to establish policy positions, whether favorable or unfavorable. It’s important for the mining industry to continue to engage and provide education and proper data so policymakers can make informed decisions.

While Texas Senate Bill 1751 sought to limit the Bitcoin mining community, many have come out in support of what miners can bring to the grid, including ERCOT CEO Pablo Vegas, U.S. Senator Ted Cruz, and Texas Governor Greg Abbott:

“In five years, I expect to see a dramatically different terrain with Bitcoin mining playing a significant role as strengthening and hardening the resiliency of the grid” - Texas Senator Ted Cruz (October 2021)

We expect regulatory pressure to continue at the federal level in the coming months as the Biden administration continues its focus against the broader sector. However, we believe there is strong opposition to many of the more hostile anti-industry policy positions.

To avoid negative outcomes, the industry must come together in an effort to further educate policy makers at the Federal level, and especially policymakers who have taken a more negative stance towards the industry. While some lawmakers are proactively defending Bitcoin and the mining industry in Congress, there is more educational work to be done ahead of the 2024 presidential election where Bitcoin could become of national interest during political conversations.

Potential Network Trends for 2H 2023

Competition for Blockspace & Emerging Fee Volatility

Over the past 6 months, the increased competition for blockspace due to the emergence of inscriptions and BRC-20s has led to a dramatic change in mempool dynamics and fee rate volatility. In this section, we cover the following:

Different classes of users with specific time preferences how they are responsible for different fee regimes that directly impact the profitability of miners.

Inscriptions and BRC-20 in particular have exacerbated the pattern of higher fees during US hours and lead to a corresponding exponential increase in transaction revenue for miners.

Rational consumers of blockspace may start to take notice of these patterns and adapt their behavior, which could have a significant negative impact on fee revenues.

Some pool pay-out schemes may become less attractive in a post-halving environment and lead to higher network centralization.

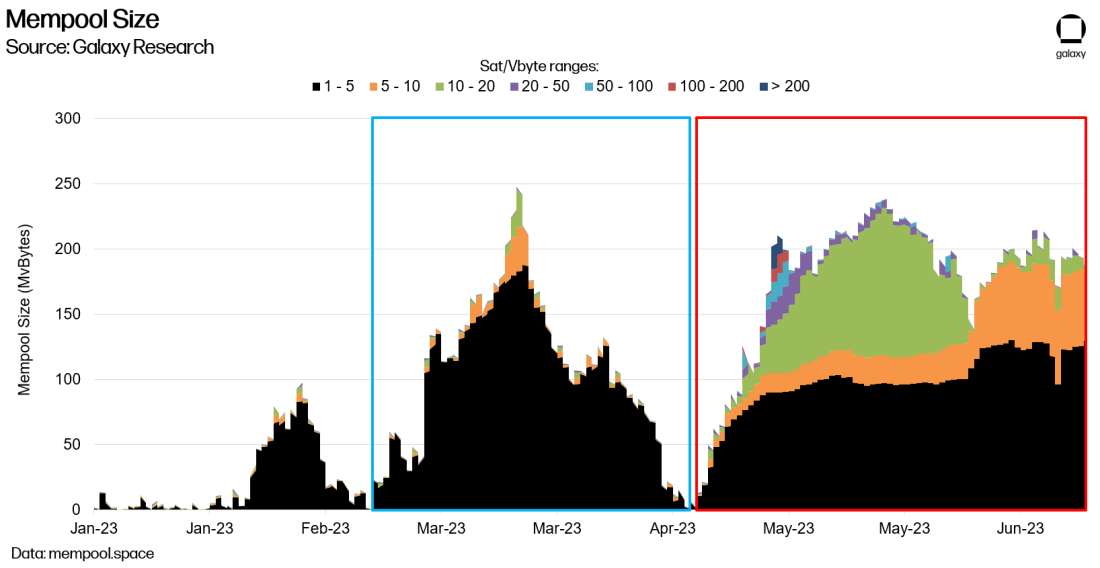

Ordinal theory and Inscriptions have introduced two new classes of blockspace consumers that have dominated the mempool in the first half of the year, pushing the mempool size to go over 1 GB of capacity (despite the default size for a regular node being around 300 MB). In the graph above, you can clearly identify these new classes, with Inscriptions users focused on trying to inscribe data on the bitcoin blockchain for the lowest cost possible, and BRC-20 users rushing to mint and trade new tokens.

The BRC-20 class (in Red in the graph above) has had a very distinct behavior from the Inscription class (in Blue). Inscribers typically have a low time preference (not in a rush to be included in a block), while BRC-20 users have more incentive to pay high fees to ensure being included in the very next block, as most of the BRC-20 activity to date has involved users participating in token mint events with limited supplies. The result is the emergence of a larger "spread" between low priority transactions and high priority transactions. This shows that BRC-20s should be considered as high value financial transactions (they also use much less blockspace) as the emergence of 50 sats/vByte feerate bands and above during May 2023 suggest.

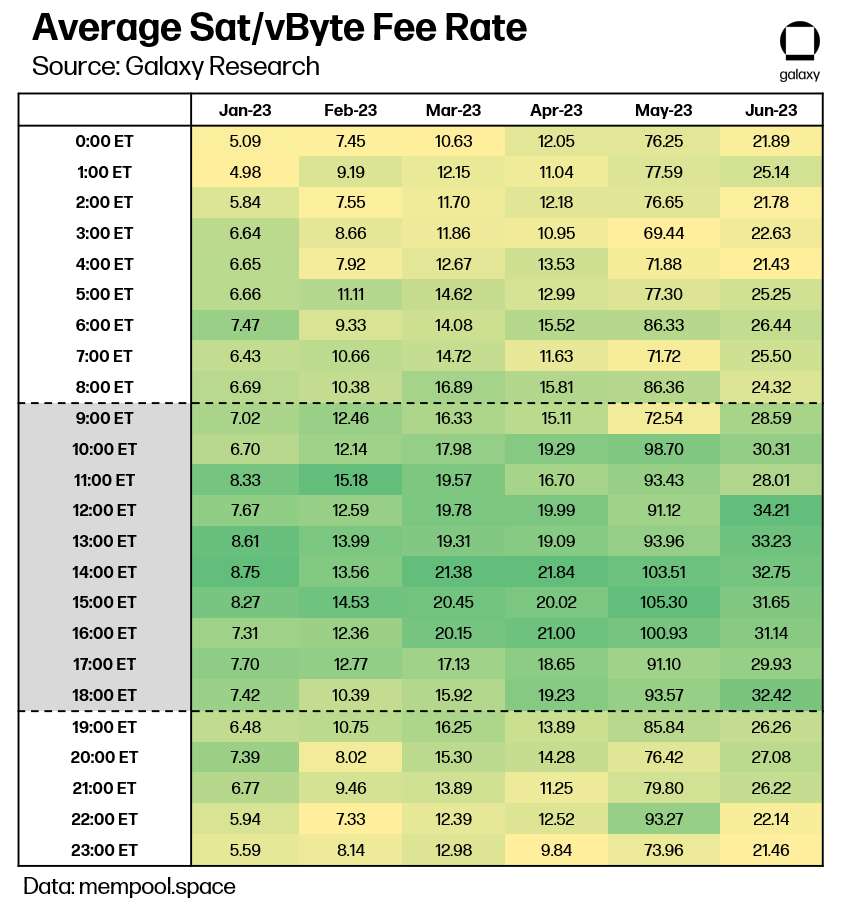

Alongside rising fees in the first half of 2023 has come an interesting trend that we have observed on the actual timing and dispersion of fee spikes in a given day. The table below shows the average of median block fees (in sats/vByte) for blocks mined in a given month and at a given hour during the day.

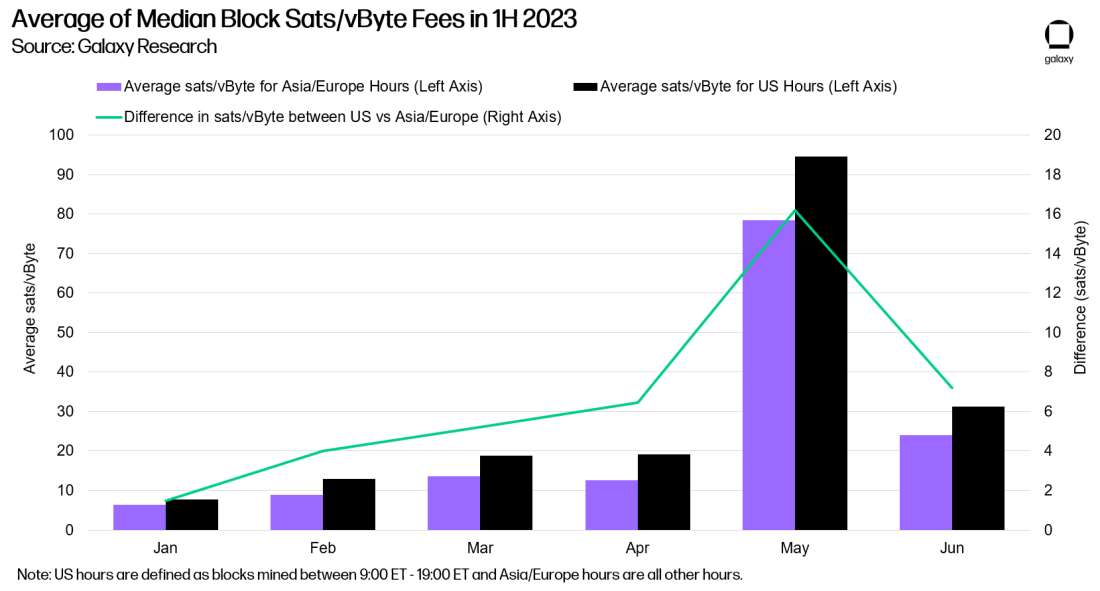

For example, the top left box (0:00 ET, Jan-23) indicates that the average of median block fees for blocks mined in Jan 2023 in the first hour of the day was 5.09 sats/vByte. Defining US trading hours as 9:00 ET – 19:00 ET shows how much fees rise during US hours and fall during Asian/European hours. The chart below further summarizes this daily fee trend by taking the average of median block sats/vByte fees for US trading hours (9:00 ET – 19:00 ET) versus Asian/European hours (19:00 ET – 9:00 ET).

While blocks mined during US hours typically have higher fees than those mined during Asian/European hours, we can also see how the run up in fees tends to drive the nominal spread between the two periods of time wider. For example, as BRC-20 activity expanded in May, the spread between US hour fees vs Asian/European hour fees widened to roughly 16 sats/vByte.

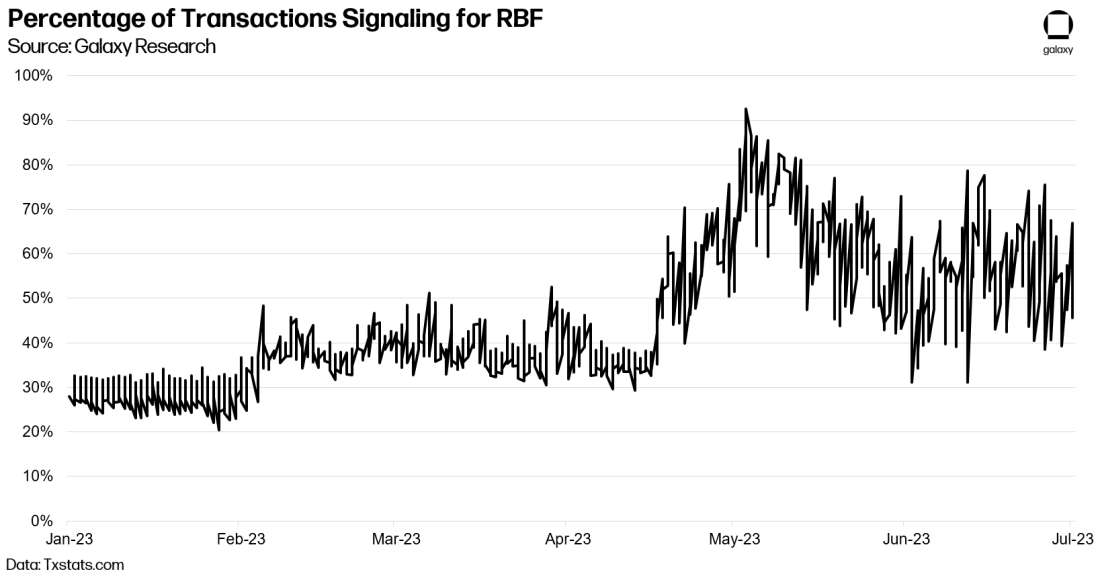

As there is a real cost to inscribing ordinals, we anticipate that users of the protocol will become more sensitive to timing of inscriptions and optimize when during the day they intend to inscribe their data to the blockchain. Especially for larger projects, this optimization could lead to meaningful savings. Like energy markets, we can expect On-Peak and Off-Peak dynamics to emerge as intense competition for blockspace will change the nature of mempool policies. For example, we can expect RBF (Replace-By-Fee) adoption to increase as more users understand the game theory of mining. During the BRC-20 craze and ever since then, RBF usage has risen moderately, indicating that the popularity of such tools is directly correlated to transaction activity on the network, which is a positive sign for miners in the long run.

We anticipate that continued ordinals experimentation will drive continued elevated blockspace demand that results in a slowly rising fee level and growing fee volatility. This shifting dynamic will put mining pools in the spotlight. Pools that pay out on an FPPS basis pay out an average of fees that are included in blocks during a 24-hour period. Fee volatility forces pools with a lower percentage of network hashrate to hold an increasingly larger treasury to avoid liquidity issues.

On the other hand, miners that opt to use pools with smaller network hashrate and PPLNS payout schemes will increase their potential exposure to bad mining luck during high fee hours. As a result, uneven network hashrate between pools will result in wider disparities in total rewards from pool payouts. Therefore, you could anticipate that rational miners will be incentivized to join the most profitable pools, which would likely be the ones with the highest concentration of network hashrate. This could in turn fuel a negative feedback loop that directly impacts the decentralization of the network at the mining level.

The fee dynamics that we witnessed in the first half of 2023 spawned a new era of fee volatility. Entering into the halving, this volatility will become even more amplified, as fees continue to climb as a percentage of miners’ total rewards. As users continue to compete for blockspace, mempool behaviors will shape different fee regimes that miners and pools will have to understand in order to remain competitive. With the halving around the corner, transaction fees increasing is a net good for miners that will improve their ability to remain profitable.

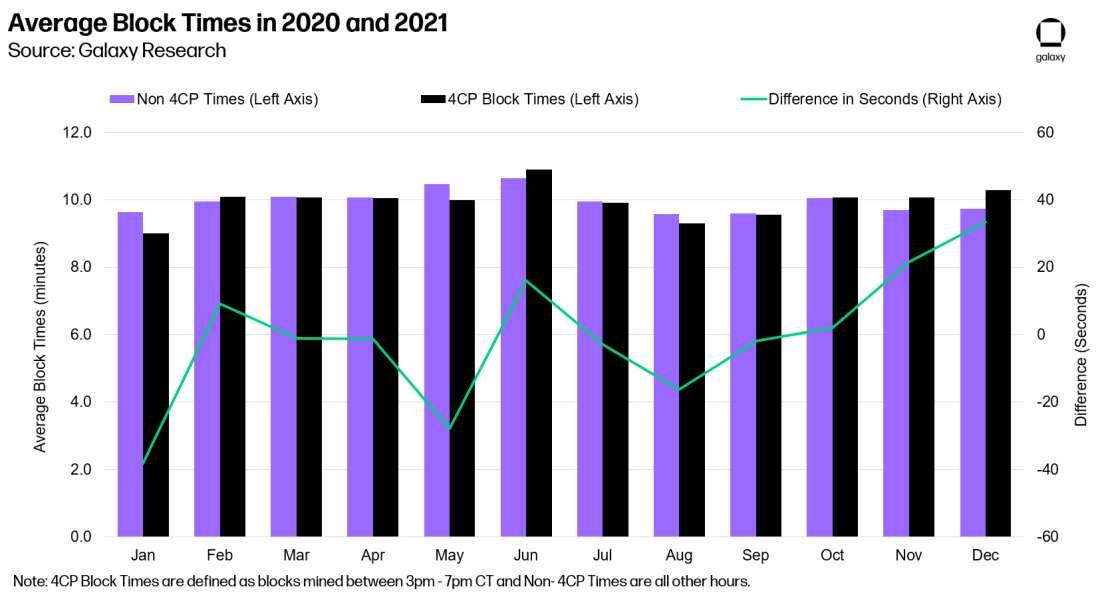

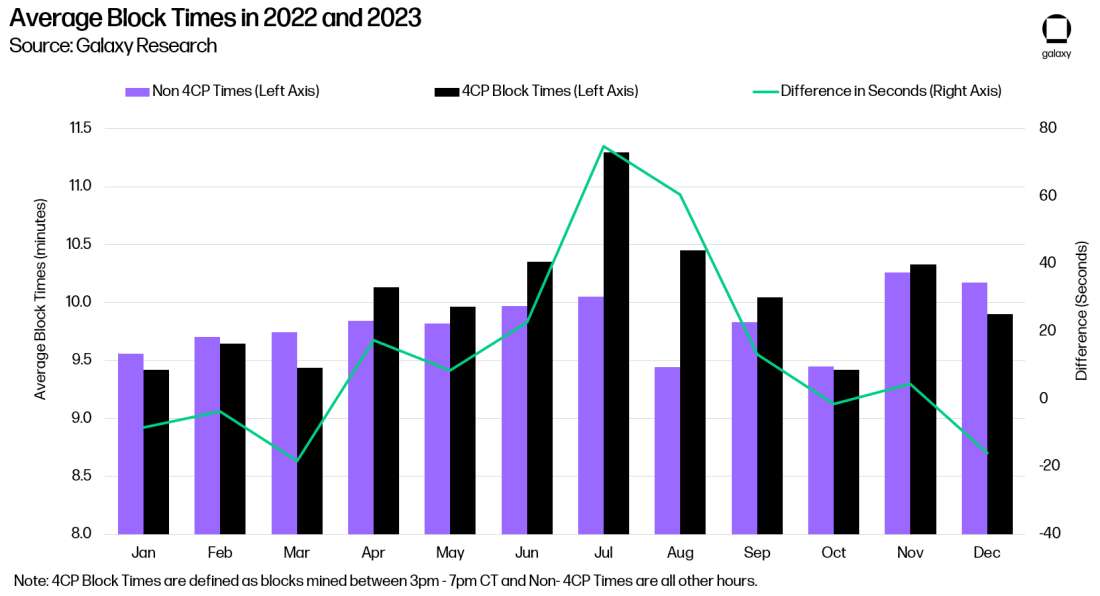

Hashrate Seasonality from 4CP & Economic Curtailment

With an increasing amount of hashrate located in Texas, currently amounting to over 2 GW of capacity, seasonal hashrate volatility is likely to rise during the summer months as ERCOT load hits its peak levels. Because miners are price sensitive, they will voluntarily curtail their operations as energy prices exceed the breakeven $/MWh price of their fleet. Seasonality is not a new phenomenon on the Bitcoin network. When Chinese hashrate represented over 60% of the network (Before May 2021), hashrate would surge during the rainy season as miners would move to the hydro rich region of Sichuan in order to profit from cheap electricity prices. Hashrate would subsequently reduce when the dry season arrived. While the context for Texas miners is different, the underlying idea remains the same: optimizing for the best economic outcomes.

In addition, miners in ERCOT also need to be responsive to the 4 Coincident Peaks (4CP) program, where ERCOT charges loads based on their contribution to overall load during the peak levels of demand in June, July, August, and September. 4CP time periods typically occur in the late afternoon in Texas between 15:00 – 19:00 CT. To avoid having to pay charges associated with being online during 4CP time periods, miners will voluntarily curtail based on forecasts during these periods of time.

As a result, hashrate is likely to reduce during these periods leading to slower block times. In summary:

Since 2022, some degree of hashrate seasonality seems to have emerged as average block times to increase during summer months (June to September).

This summer seasonality can be in part explained by the increasingly large percentage of Texas miners coming offline as a direct result of economic curtailment and 4 CP operations.

We expect this seasonality to become more pronounced as miners continue to refine their power strategies and curtailment operations, which would lead to greater hashrate volatility, directly impacting mining profitability.

The below charts show the block times were historically during 4CP times (15:00 CT – 19:00 CT) versus all other hours. The green line depicts the difference in 4CP block times versus all other hours (in seconds). In 2020 and 2021, there wasn’t nearly the same concentration of miners in ERCOT compared to 2022 and 2023 and as shown below, there was a dispersion in block times during the summer months, without any real trend.

In 2022 and 2023, as miners developed more operations in ERCOT, we have seen this trend play out. Specifically in July and August, when peak demand reaches its limits, we can see that 4CP block times slow down, to over a 60 second difference, indicating some degree of seasonality.

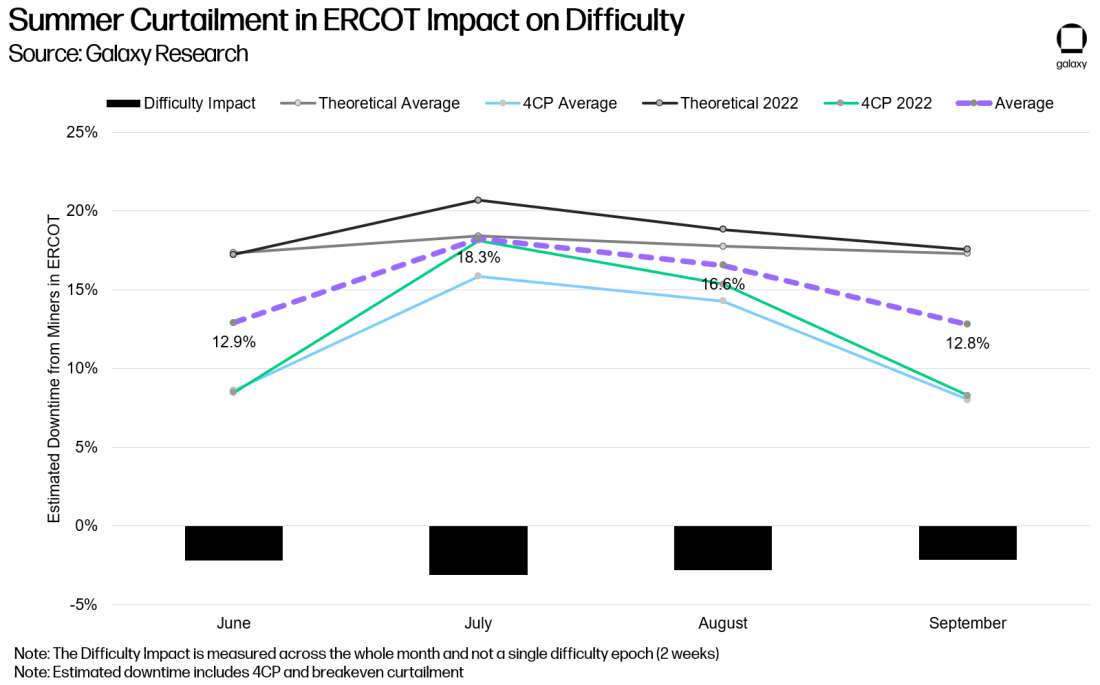

The implications of this slowdown in block times can be explained in summer months in part because of 4CP (4 Coincident Peaks) activity in Texas and higher peak power prices. The analysis below tries to calculate the estimated amount of downtime for Texas miners over the 4CP period and the corresponding impact on difficulty.

With the assumption that 17% of network hashrate (or roughly 2 GW of capacity) is located in ERCOT, we estimate that on average miners in ERCOT are offline around 12.9% of the time in June representing a negative 2.2% impact on difficulty over the month. Peak downtime happens in July, when miners could be offline for more than 19.4% of the time, representing a negative 3.3% impact on difficulty. These estimates were calculated by adding up the amount of time miners have been offline historically due to economic curtailment when power prices were above their marginal breakeven cost to mine (we chose $150/MWh for this analysis), and the amount of time they would be offline due to 4CP avoidance. The theoretical scenario assume that miners would be offline 100% of the time during 4CP hours (4 hours per day representing a 17% downtime for the month plus downtime from economic curtailment) while the 2022 scenario assumes that this year will be similar to last year (i.e. A volatile year for the grid that would lead to higher peak prices and similar peak avoidance behaviors that would be closer to 4 hours per day).

Based on the historical analysis of average block times during the summer and the specific behavior of ERCOT miners during 4CP months, we can confidently assume that there will be an increasing correlation between 4CP and network hashrate volatility. Just like the rainy season would boost Chinese miners hashrate before the ban in 2021, miners in Texas have a similar impact on the network except that they contribute to a temporary slowdown of hashrate growth over the summer months. While global network hashrate growth during summer months will be slowed by 4CP and economic curtailment, we also expect that in the months just after 4CP there will be a spike in network hashrate due to higher uptime from miners in ERCOT.

Going forward, we expect this seasonality to increase as miners continue to expand operations in Texas and become even more sophisticated in their power strategies.

What to Expect from Bitcoin's 4th Halving

Bitcoin’s fourth halving event is expected to occur sometime around April 2024. Every 210,000 blocks (approximately every 4 years), the Bitcoin network automatically halves the per-block issuance of newly minted bitcoin. This process is what ultimately results in Bitcoin’s fixed terminal supply of 21m coins. But given that the block subsidy (the newly minted issuance) comprises the majority of miner revenue, the halving is an important event for the mining industry with potentially wide-ranging impact.

How Public Miners Prepare for the Halving

With the halving less than 10 months away, miners have enacted several strategies to position for the event.

Fleet Upgrades: For the miners that have a better liquidity profile and been able to raise capital to some degree, many have invested in the latest generation of machines. Miners that are higher on the power cost curve have also opted to try and upgrade their fleet to more efficient machines to put themselves in a better position to be competitive post halving.

Mergers & Acquisitions: For the public miners that find themselves in a more challenged position due to a combination of either high power costs, lack of a growth story, desire to vertically integrate, or an inability to raise, M&A has been an attractive option. In this way, miners have been able to find synergies with companies that bring something to the table to make up for their existing shortcomings.

Revenue Diversification: Several public miners have either announced intentions or have already actively taken steps to participate in the high-performance computing (HPC) datacenter space, thereby diversifying their revenue streams. The HPC space presents miners with an uncorrelated revenue stream to bitcoin mining while simultaneously being able to take advantage of the massive hype around AI computing.

Potential Hashrate Could Come Offline

A recent study conducted by Karim Helmy (formerly of Galaxy Research) and Coin Metrics showed that roughly 30% of network hashrate is made up of M20S, M32, S17, e12+, A1066, A1246, and S9 machines. With network hashrate at roughly 369 EH as of June 30th, the implied contribution to network hashrate coming from this group of machines is 110 EH. Given that these machines are less efficient, it is reasonable to assume that the makeup of these machines within the network will remain relatively fixed up until the halving. If we assume of the 110 EH that these machines represent that 90% of these machines will be turned off due to becoming unprofitable, that will represent a 99 EH loss.

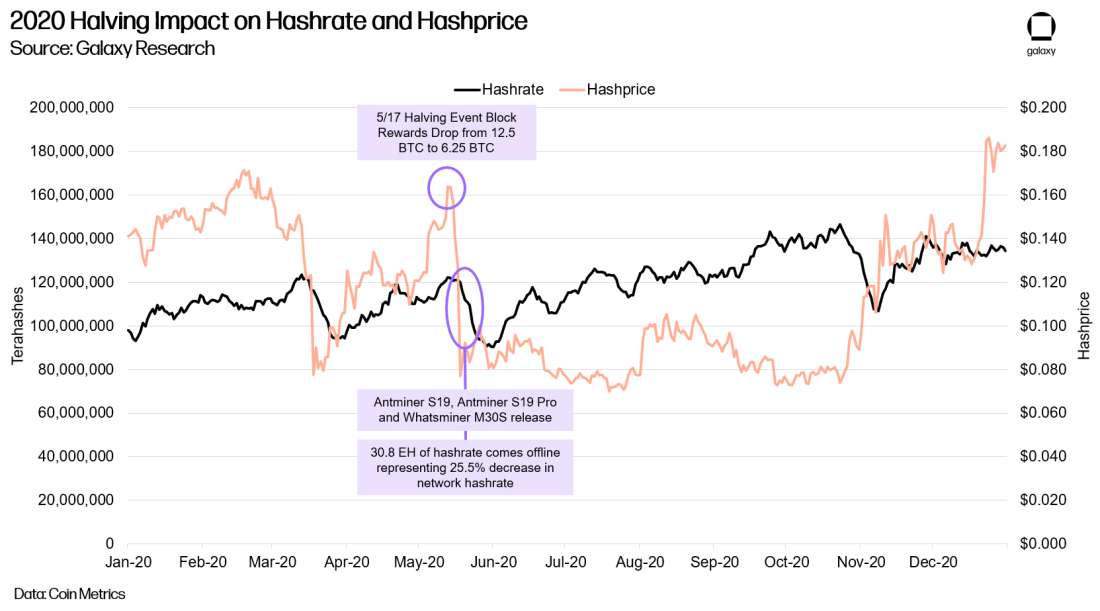

If network hashrate reaches 500 EH by the time of the halving that 99 EH loss would reflect a 19.8% loss in network hashrate. When looking back at the 2020 halving, a 20 – 30% loss in network hashrate seems plausible as 25.5% of network hashrate, representing 30.8 EH of hashrate, came offline following the halving. A majority of the lost hashrate during the 2020 halving was from S9's that were no longer profitable. During the same month as the halving, Bitmain launched the S19 and S19 Pro and MicroBT launched the M30S. As a result, network hashrate made a fairly quick V-shaped recovery and reached new all-time highs in just 55 days even while hashprice remained near all-time lows (ranging between $0.07 - $0.10).

Given this, it does not seem farfetched to expect to see a similar V-Shape recovery in network hashrate post the 2024 halving. Much of the loss in network hashrate coming from less efficient machines will be quickly offset by new M50 series and S19 XP series machines being energized. Several publicly traded miners have already announced large ASIC futures orders of M50 series and S19 XP series machines with anticipated deliveries in Q1 and Q2 of 2024. It is also highly likely that MicroBT, Canaan, and Bitmain with announce another improved ASIC in their current series of machines around the time of the halving. The key wildcards that will have a significant influence on these outcomes of course are energy prices and specifically what happens with natural gas and bitcoin price. Assuming natural gas remains at current levels and bitcoin price is able to stay above $30,000 or even continue to trend slightly higher a V-Shape recovery in network hashrate seems to be the most probable outcome.

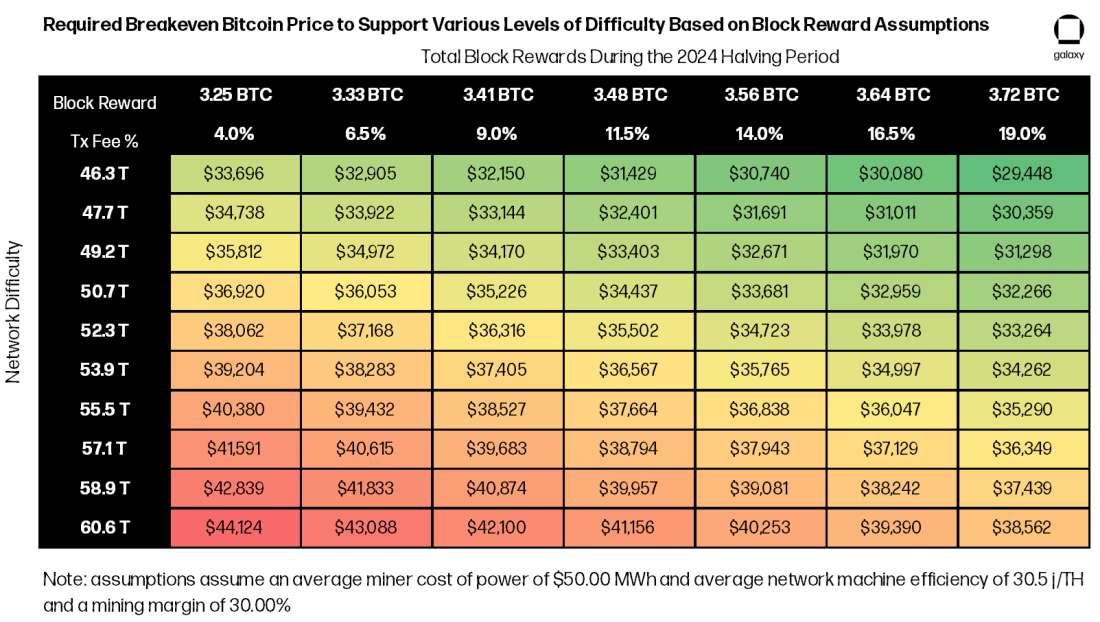

How Much Hashrate Can the Network Bear Post Halving

To try to understand how much hashrate the network could bear, we created a series of sensitivity analysis to try to understand the bitcoin price that would ultimately be required to sustain certain levels of hashrate given a few key assumptions:

An average miner cost of power of $50 per MWh

Average network efficiency of 30.5 j/TH representing majorly S19j Pro machines making up the post halving average machine efficiency

Price required for miners to earn a 30% gross mining margin, which is equivalent to a $71 per MWh breakeven.

Note that network difficulty as of June 30th stands at roughly 50.6T. Given the assumptions above, if bitcoin’s price ranges between $30,000 and $35,000 a majority of miners in the network would still be able to operate profitability with a healthy gross margin even at current network difficulty levels (which currently imply 375 EH of network hashrate). It’s also interesting to note the level of impact increased transaction fees can have on lowering the effective breakeven bitcoin price necessary to sustain profitability at various levels of network hashrate.

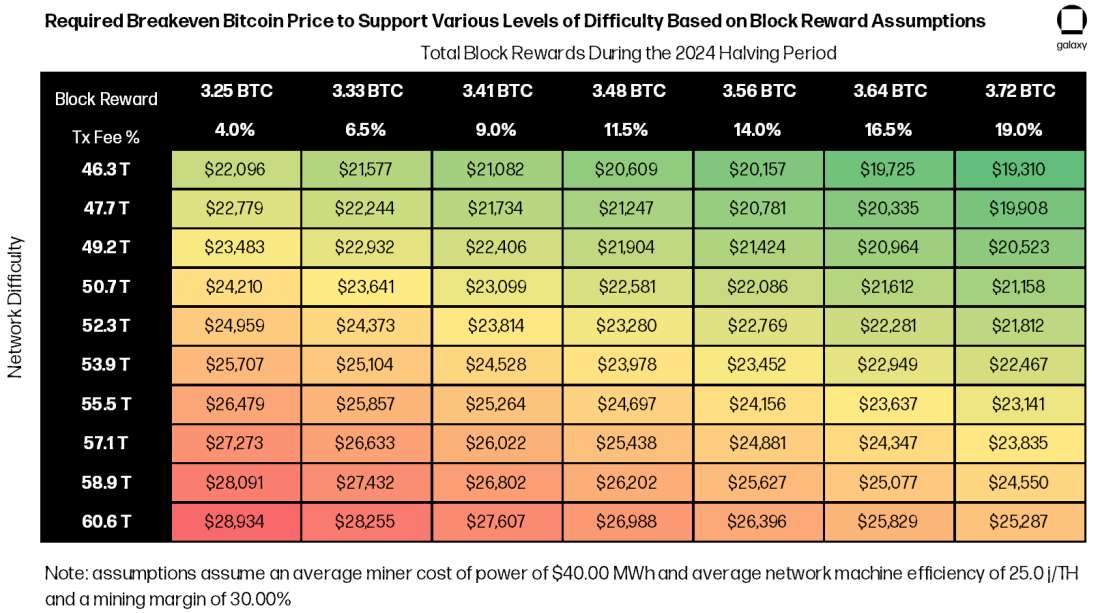

Leveraging this same analysis but with more aggressive assumptions for the average cost of power and efficiency of machines, the necessary bitcoin price required to sustain various levels of network hashrate declines ~50%. Key assumptions:

An average miner cost of power of $40 per MWh

Average network efficiency of 25.0 j/TH representing an average efficiency of S19 XP and S19j Pro machines

Price required for miners to earn a 30% gross mining margin

A different analysis in which we observe the breakeven $/MWh of various ASIC models assuming a $40,000 bitcoin price and transactions at 15% of block rewards shows that even at current network hashrate levels the most efficient ASIC, the S19 XP, marginal revenue is barely above $100. As a result, the halving will put even more emphasis on miners’ power strategies and how they optimize between floating index and forward hedges. The other likely outcome is that miners who are floating 100% index pricing will experience more downtime than they have historically. This phenomenon would likely contribute to increased network hashrate volatility as we go forward.

Conclusion

Following the perfect storm that miners faced at the end of 2022, the storm as finally started to pass. While miners have enjoyed higher bitcoin prices, increased transaction fees, and lower energy costs, the rampant increase in network hashrate has offset many of these benefits. As a result, hashprice has remained in a fairly tight range between $0.065 and $0.08. With energy prices significantly lower from 2022 highs thanks to a deep decline in natural gas prices, the breakeven hashprice for the network likely stands below $0.05. Given this, network hashrate will continue to trend higher in the second half of the year as public and private miners look to add hashrate from next generation machines such as the S19 XP and M50 series.

Miners are taking several measures to prepare for the 2024 halving. A handful of miners announced plans to diversify out of the mining industry into spaces like high-performance computing to provide more stable decorrelated cash flows. There’s also been a flurry of M&A predominantly from miners who are ill-positioned for the upcoming halving. M&A has made sense for miners who either are not vertically integrate or lack a growth story or an ability to raise capital to fund new growth.

Glossary

Network Hashprice - Network hashprice, often simply referred to as hashprice, is a measure of dollar-denominated daily expected revenue from mining with a single terahash per second of hashrate on a daily basis given current conditions around bitcoin price, block rewards and network hashrate.

Sats per TH - Is a measure of bitcoin-denominated daily expected revenue from mining with a single terahash per second of hashrate on a daily basis given current conditions around block rewards and network hashrate. 1 satoshi represents one one-hundred millionth of a bitcoin.

Operational Breakeven Cost - Operational breakeven cost attempts to quantify all recurring expenditures that require a true cash outlay and includes cost of revenues, selling, general, and administrative (SG&A) expenses, and interest expenses, while excluding all non-cash expenses such as employee stock-based compensation and depreciation and amortization.

Network Hashrate - The network hashrate is the cumulative processing power of mining machines securing the network.

Ordinal – A serialization methodology for individual satoshis following “Ordinal Theory”

Inscription – An inscription is the arbitrary data stored in the witness field of a transaction.

Block Subsidy - The block subsidy is the amount of new bitcoin minted in each block. The block subsidy halves every 210,000 blocks (roughly every 4 years) according to Bitcoin’s issuance schedule and is currently 6.25 BTC.

Transaction Fees - Blocks can contain many transactions with fees attached to incentivize their confirmation and prevent spam. In addition to the block subsidy, miners also receive the transaction fees for all of the transactions included in the block that they mine.

Block Reward -The block reward is the combination of the block subsidy and all transaction fees paid by transactions in a specific block.

Hashrate - Hashrate is a measure of the computational power per second used when mining.

Power Draw - Power draw is a measure of the amount of electricity consumed to operate an ASIC or mining machine per hour.

Mining Pool - A mining pool is a middleman that aggregates multiple miners’ hashpower. Mining pools aggregate pool members’ hashes, submit successful proofs of work to the network, and distribute rewards to contributing miners proportionately to the amount of work performed. Mining on a pool reduces payout variance for miners, who would otherwise have to deal with significant risk from finding blocks at unpredictable intervals.

Terahash - A terahash (TH) is one trillion hashes, which is equivalent to making one trillion guesses at solving the puzzle to add the next block to bitcoin’s blockchain. The hashrate of most mining rigs is measured in terahashes per second (TH/s).

Exahash - A exahash (EH) is one quintillion hashes, which is equivalent to making one quintillion guesses at solving the puzzle to add the next block to bitcoin’s blockchain. The total network hashrate is typically measured in exahashes per second (EH/s), as is that of some large mining operations.

Legal Disclosure:

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsementof any of the digital assets or companies mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email contact@galaxydigital.io. ©Copyright Galaxy Digital Holdings LP 2023. All rights reserved.