Top Stories of the Week - 1/19

This week in the newsletter, we write about a fascinating new Bitcoin Ordinals collection called Quantum Cats, the latest on Ethereum’s next upgrade, and developments in the SEC v. Coinbase case.

Subscribe here and receive Galaxy's Weekly Top Stories, and more, directly to your inbox.

Quantum Cats Aim to Revive One of Bitcoin’s Original Features

Taproot Wizards is launching a new Ordinals collection called Quantum Cats this month as a way to advance a pending Bitcoin Improvement Proposal (BIP) implementing OP_CAT. OP_CAT was an original scripting function on Bitcoin included by Satoshi and removed in 2010. Bitcoin developers removed the opcode because it enabled the construction of data intensive scripts that could burden the computational resources of Bitcoin nodes. In simpler terms, it could burden the bitcoin network and disrupt its operation.

In October 2023, Bitcoin researcher Ethan Heilman put forth a BIP to re-introduce the feature (refer to our report Technical Developments in Bitcoin – Q4 2023 for more details). Adding OP_CAT back to Bitcoin’s scripting language will further enhance Bitcoin’s programmability by eliminating previously imposed restrictions and thereby creating new opportunities for diverse use cases. It improves the ability to build programs on top of bitcoin through Layer-2s and bridges by giving developers the ability to construct and evaluate Merkle trees and other hashed data structures in tapscript, the native scripting language used to enable new transaction types as part of the Taproot upgrade.

Taproot Wizards CTO Rijndael published a long thread explaining all the bitcoin and ordinals technology used in the collection. Quantum Cats takes advantage of several innovative Ordinal features to introduce a new “Evolving Inscription” feature. These primarily include Ordinal Recursions, Pre-signed Transactions, Symmetric Cryptography, and Client-side Load-Management. Collectively, this enables the cats and their artwork to change overtime in a deterministic way as the OP_CAT proposal goes through the Bitcoin governance process. For a full overview of the technical mechanisms behind Quantum Cats refer to this thread.

The Quantum Cats launch comes amidst a broader surge in Ordinals activity, which saw $1.8 billion total volume in 2023, only second to Ethereum NFTs. Taproot Wizards raised $7.5 million in seed funding last year.

OUR TAKE:

Quantum Cats fuses innovative inscription technology with advocacy for greater awareness and education of a key proposed Bitcoin upgrade and the Bitcoin Improvement Proposal (BIP) in general. At the moment, there is no OP_CAT BIP, although one has been proposed. Promoting the education of BIPs is important as discussions surrounding BIPs are extremely technical. Standard track BIPs that would require a soft fork demand heightened education and levels of consensus. Open conversation, education, and the ability to signal support for major Bitcoin upgrades is a big part of how consensus is built for new upgrades.

Taproot Wizards are calling for re-instating OP_CAT and have designed their Quantum Cats Ordinals collection around this initiative. The selling of social signaling attire or collectibles is not new -- in fact Quantum Cats looks a lot like the UASF hats worn by SegWit supporters in 2017. But the use of Ordinals -- effectively NFTs -- and particularly ones that are so advanced from a bitcoin and ordinals technology perspective, adds a fascinating new twist.

The project is also raising discussions about the BIP process itself. Along with the Quantum Cats collection, the Taproot Wizards also release BIP Land, a board game that satirizes the complexities and pitfalls of the BIP process, which Blockstream CEO Adam Back said “impressed” him. There is no actual requirement that any Bitcoin upgrade formally present itself as a Bitcoin Improvement Proposal, though that has been the convention. But the BIP process - the format, the assignment of BIP numbers, the addition to the BIP repository - is effectively controlled today by one developer: Luke Dashjr (who, incidentally, is one of Taproot Wizards’ main antagonists). Taproot Wizard co-founder Udi Wertheimer, among others, has been critical of the BIP process for a while, and some bitcoin developers are beginning to agree that it needs revamping. While technically there are two devs who maintain the BIP repository, only Luke Dashjr has ever merged a BIP proposal. Anthony Towns, a bitcoin core developer and maintainer of Bitcoin Inquisition (a testnet for new bitcoin upgrades), wrote to the bitcoin-dev mailing list Wednesday agreeing that the current BIP process is “very high friction.” Luke Dashjr himself wrote back to Towns and suggested that perhaps a BIP 3 is warranted (1 and 2 describe the BIP process, and then the first substantive BIP is BIP 8, with 3-7 reserved for consequential or process-related BIPs), though he disputed Towns’ general complaints about the BIP process. Rob Hamilton, CEO of Bitcoin custody and insurance company AnchorWatch, told Alex in Nashville Thursday that “seeing recent discourse around BIPs, and how to suggest consensus changes in Bitcoin, migrate to the mailing list is a healthy development in the developer ecosystem.”

The emergence of the OP_CAT campaign could motivate Bitcoin developers to begin seriously considering other BIPs or the BIP process in general. If leveraging Ordinals to educate and advocate for BIPs proves to be a successful method for expediting or overhauling the BIP process, it is reasonable to anticipate that proposals closer to inclusion, such as BIP 119, BIP 118, and BIP 345, could also benefit. If Quantum Cats manages to both educate about Bitcoin technology and contribute to the development of a specific upgrade, it would be a groundbreaking and impactful endeavor. Even if it only achieves the former while innovating within the Ordinals ecosystem, the project remains fascinating and thoughtful, driven by a profound love for Bitcoin at its core. - Alex Thorn, Gabe Parker, Lucas Tcheyan

Ethereum Devs Push Forward on Upgrade Despite Hiccup

On Wednesday, Ethereum developers activated the Cancun/Deneb (Dencun) upgrade on Goerli, the largest multi-client public Ethereum test network. The upgrade immediately resulted in the loss of network finality as a large percentage of node operators failed to follow the canonical Goerli chain. This was due to a bug in the Prysm client, the most popular consensus layer (CL) client run by validator node operators on Ethereum. As explained by Prysm developer Terence Tsao on All Core Developers Execution (ACDE) #179, the issue in the Prysm client stemmed from an empty historical roots field that went unchecked on prior devnets and shadow forks testing the Dencun upgrade.

As background, the historical roots field is a legacy field from the Shanghai/Capella (Shapella) upgrade that represented a part of the Beacon Chain state that nodes could update less frequently than other parts of the Beacon Chain state. During prior devnets and shadow forks testing Dencun, the historical roots field was not adequately tested in Prysm validators due to the speedy cadence through which these prior test networks activated historical upgrades like Shapella. However, on Goerli, a longstanding Ethereum testnet that has been upgraded according to a similar timeline as Ethereum mainnet, the empty value in the historical roots field a temporary chain split as Prysm validators dropped off from the network. Within four hours of Dencun activation on Goerli, the Prysm team issued a hot fix to their client, which resolved the low participation rate from validators on Goerli and resulted in the network being able to finalize transactions and blocks once more.

Since Goerli node operators implemented the hot fix to their Prysm nodes, the Goerli network has remained stable. However, as discussed on ACDE #179, there does not appear to be any L2 protocols testing their infrastructure and tooling for the Dencun upgrade on Goerli. The primary code change in the Dencun upgrade is EIP 4844, which is aimed at reducing L2 transaction fees. A representative from the Optimism team on the call said that they may be ready in two to three weeks to test their support for the upgrade on Goerli. Despite the lack of insight on the use of Dencun by L2s, developers agreed to push forward with the activation of Dencun on the Sepolia and Holesky testnets, the last two public testnets on Ethereum that will be upgraded before Ethereum mainnet, posthaste. Sticking with the timelines shared on ACDE #177, Sepolia will be upgraded on January 30 and Holesky one week thereafter on February 7. The client releases for both testnet upgrades will be identical, though at least one client team, the Lighthouse client team, has indicated the possibility that their client release for Sepolia and Holesky may not be the one recommended for use on mainnet.

Assuming a somewhat stable activation of Dencun (even one that results in a chain split so long as the issue is quickly addressable through a hot fix) on both Sepolia and Holesky, developers may decide to activate Dencun on Ethereum mainnet shortly thereafter. Ethereum Foundation Researcher and Chair of the ACDC calls Danny Ryan suggested that developers could activate Dencun two to three weeks after the Holesky upgrade, which would mean Dencun is activated on Ethereum by the end of February.

However, as pointed out by “Protolambda”, a pseudonymous developer working on the Optimism L2 protocol, this timeline may be faster than L2s can support. Protolambda indicated that his team would not likely be able to support Dencun on mainnet until late March or early April.

OUR TAKE:

Ethereum core developers are moving faster than expected with the activation of Dencun on public testnets despite multiple reasons for a potential delay to the testnet upgrade timeline such as the need for a hotfix to a major client after the activation of Dencun on Goerli, the lack of mainnet ready client releases for Dencun from all major client teams, and the lack of readiness from L2s to support the upgrade on any testnet, let alone mainnet.

The rationale from certain developers expressed on this week’s ACD call was that the issue in Prysm discovered on Goerli was an easy enough fix that did not require further analysis. However, there were important learnings from the bug that will impact testing for future Ethereum upgrades. It was also a significant enough issue that validators on Goerli could not finalize the network until the bug was fixed. Despite the easy solution, the nature of the bug was not inconsequential and if it had been caught on mainnet, would have disrupted applications and end-users on Ethereum.

One of the key reasons why this bug was not caught earlier in the Dencun testing process is due to the speed at which developers ran through testnet activations of Dencun on prior testnets without waiting or allowing for sufficient time for key milestones and events to be triggered on these networks. As noted in prior newsletters, the complexity of the Ethereum protocol has increased greatly since the activation of the Merge and Shanghai upgrades. Finding bugs in code is becoming more like trying to find a needle in a haystack due to the complexity of protocol. Thus, while it is expected that bugs, like the one seen in the Prysm client this week, are still discovered more than two years into testing the upgrade, it should also be expected that the time to test these upgrades increases the more persistently major client releases fail to be mainnet-ready.

Further, while certain developers are of the opinion that Ethereum can and should move more quickly in adopting code changes that are ready for implementation without waiting for the readiness of L2s, the motivation for doing so is weak considering the benefits of more robust testing time for the upgrade with mainnet-ready releases from all major client teams and the simple fact that the main motivation for Dencun, unlike prior upgrades, is better supporting L2s. If the very target users that will be benefitting from the Dencun upgrade are L2s and little to no L2s are presenting themselves as ready to support this upgrade, which is the case right now, the urgency felt by developers to blaze forward with their ambitious timeline for Dencun testnet upgrades is odd and frankly, confusing. Allowing for the main beneficiaries of this upgrade to sufficiently test their infrastructure for the upgrade before the upgrade happens would seem reasonable. For more insight on sentiments shared by developers about the readiness of the two largest L2s on Ethereum, Arbitrum and Optimism, for Dencun, read this week's ACD call notes.

It would appear L2 teams are more conservative than Ethereum protocol developers in their estimations for supporting Dencun because of upgrade complexity and lack of sufficient infrastructure and tooling to support its use. Based on the value and maturity of L2 protocols compared to Ethereum, you would think it should be the other way around.

So, given the fervor of Ethereum core developers to ship Dencun seen in the aftermath of the Goerli fork this week, the likelihood of Dencun implementation on Ethereum mainnet by the end of March is likely around 60% in this writer’s opinion. The likelihood of an Ethereum mainnet upgrade even earlier by the end of February is unlikely, roughly 30%, because while developers are clearly bold, they’re not crazy. Finally, there remains a non-zero chance that Dencun is pushed out past March to April or further, if developers discover an unexpected and serious enough bug in the Dencun upgrade on Sepolia or Holesky, which is scheduled to be upgraded on January 30 and February 7, respectively. Timeline estimations for Dencun mainnet activation should be updated in accordance to how the Dencun upgrade goes on these two respective testnets. - Christine Kim

SEC & Coinbase Have a Day in Court

On Wednesday, the Southern District heard oral arguments in Coinbase’s motion to dismiss (MTD) the suit brought by the Securities & Exchange Commission. On Wednesday January 17, Federal Judge Katherine Polk Failla heard arguments from Coinbase and the SEC regarding Coinbase’s motion to dismiss. The SEC alleges that 13 tokens traded on Coinbase are themselves unregistered securities. Additionally, the SEC alleges that Coinbase’s staking service, in which users can stake ETH through Coinbase’s staking nodes, is also an unregistered security. Coinbase argues that the trading of the specified tokens are secondary market trades in which no “investment contract” exists between issuers and investors and, thus, they cannot be securities.

One interesting line of questioning of Coinbase from Judge Failla revolved around the major questions doctrine (MQD), which outlines that courts will presume that Congress does not delegate to executive agencies issues of major political or economic significance. In the context of this case, Coinbase has argued that the securities law status of crypto assets should raise the major question doctrine and, thus, Congress should act, not the SEC. Senator Cynthia Lummis filed an amicus brief in favor of Coinbase on this topic, in which she stated “the SEC brings this enforcement action in the midst of debates in the halls of Congress and around the world about how crypto assets should be regulated. The Constitution empowers Congress—not the SEC—to legislate in such an area of profound economic and political significance.” Coinbase argued that MQD is not triggered because of the technological innovation of digital assets in this case, but that the novel class of transactions the SEC is attempting to regulate (i.e. secondary market transactions of cryptocurrencies constitute sales of investment contracts) does. The judge referred to MQD as the “nuclear option” and feared that in triggering it she would be stepping out of her realm of responsibility and into that of another branch of government; which she expressed is something Coinbase is accusing the SEC of doing.

A major point of disagreement between the two parties was in the application of the Howey Test to the coins in question. The SEC took the stance that Coinbase is creating its own version of the Howey Test in an attempt to circumvent “the carefully constructed regulatory structure” crafted by the Congress of 1934. Coinbase’s lawyer, on the other hand, argued that “there would have been a lot of surprise in the 1933/1934 Congress to find an investment contract didn't have anything to do with a contract at all” and that the SEC’s application of the Howey Test in the context of their complaint brings the court into “unprecedented territory.” Another highlight from the hearing was the SEC’s acknowledgement that the coins in question are “not securities in and of themselves” and are “just lines of code.”

Coinbase lawyers are hopeful the judge will toss out the SEC’s case against the exchange, but we will have to wait for several weeks or even months before the court rules on the MTD.

<strong>OUR TAKE:</strong>

SEC v. Coinbase is a monumental case that can have a profound impact on how crypto is regulated in the US. The SEC hopes to expand its oversight over the industry by applying the Howey Test to certain crypto assets - an approach it has pursued for years to achieve enforcement victories, but which has only just recently begun being tested in court. Also in the same federal court, the Southern District of New York (SDNY), last summer Ripple won a partial victory against the SEC when Judge Torres ruled that airdrops and secondary market transactions of XRP were not securities (though institutional sales were). Then, also in SDNY a few weeks later, Judge Rakoff ruled that a variety of types of tokens in the LUNA ecosystem were securities, effectively rejecting Torres’ analysis in Ripple. Now a third Judge in the same building, Judge Failla, is hearing another major consequential case. Failla grilled lawyers from both sides in a balanced line of questioning, showing advanced understanding of the issues at hand.

Importantly, the SEC admitted that digital assets aren’t in and of themselves securities, but the transactions of them on secondary markets can constitute investment contracts. Coinbase has argued that the SEC is attempting to regulate crypto without a limiting principle. This approach, in effect, gives the SEC authority to regulate anything with a market price that trades on a secondary market (e.g. baseball cards selling on Ebay, concert tickets on Stubhub, or furniture on Facebook marketplace).

We believe that cryptocurrencies are fundamentally novel and, while some may be securities, they fundamentally do not fit within current US securities regulatory frameworks. There are effectively two paths regulators can take to bring clarity to digital assets on this topic: 1) create a new, bespoke regime starting from first principles (which is the approach the EU has taken with its Markets in Crypto Assets (MiCA) regulation), or 2) fit digital assets into existing regulatory frameworks (the approach the United Kingdom has been taking). The first approach is certainly valid if done deliberately in a way that balances capital formation and promoting innovation with consumer protection and orderly markets. The latter can also be effective, but requires the production significant interpretive guidance so existing regulated entities understand how to apply old rules to new technologies, asset classes, or processes. The SEC has taken the latter approach but has neglected to produce substantive guidance on how entities like broker/dealers, exchanges, transfer agents, or others could actually custody, list, trade, or use digital assets. To date, only one broker/dealer has been approved to interact with digital assets by the SEC, Promethean, but has admitted to not actually having begun trading or interacting with any digital assets, including bitcoin.

It is unfortunate that the industry has had to receive more clarity from courts than from regulators who could have worked with industry to develop reasonable frameworks rather than pursuing a costly and potentially disastrous (for both the defendants AND the SEC) litigation strategy. We expect Judge Failla to publish a ruling on Coinbase’s MTD within 3 months. -Alex Thorn, Zack Pokorny

Charts of the Week

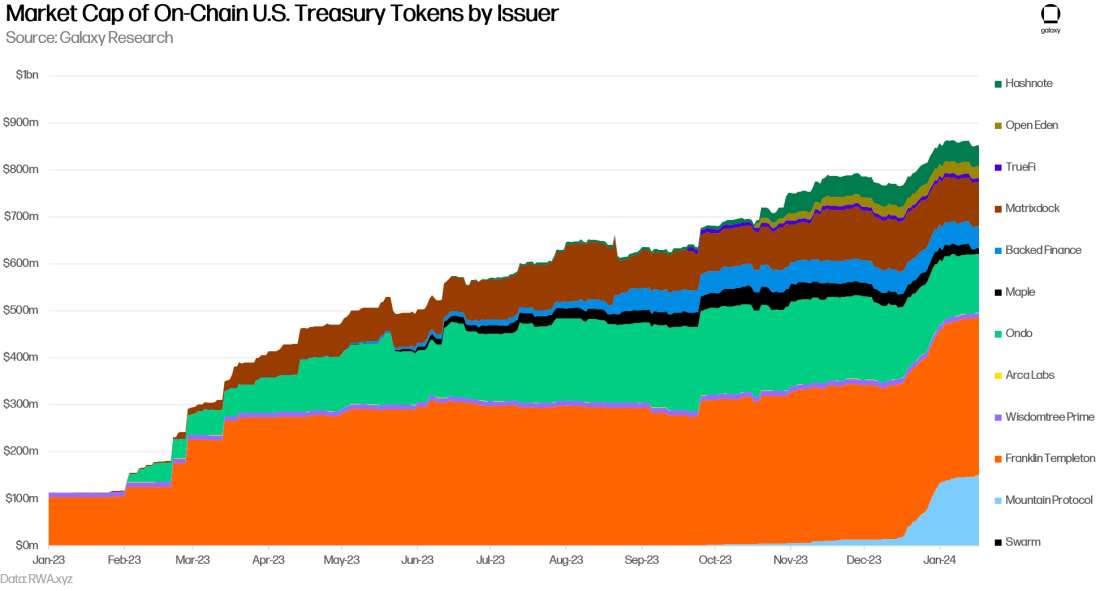

The market capitalization of tokenized U.S. Treasury Bills on-chain is seeing strong growth even as the Fed has signaled that rates are sufficiently high enough. They have added $66m (+8%) to their market cap over the last 30 days. Franklin Templeton is the largest issuer of onchain T-Bills, holding a dominance of 40%.

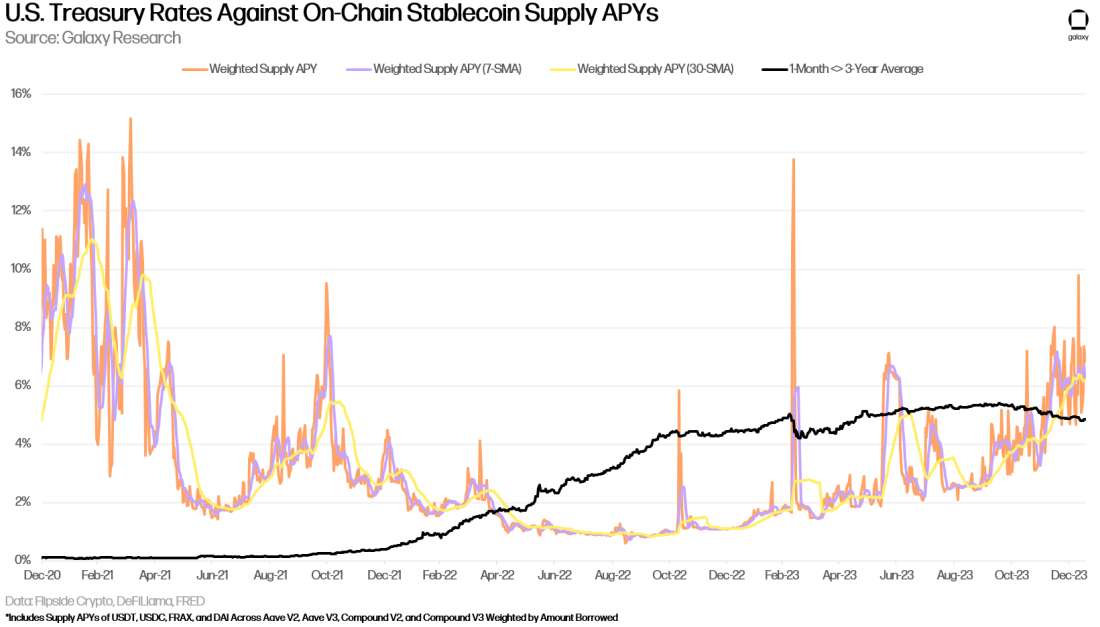

The growth also comes as competition from onchain rates heats up. Stablecoin lending (supply) rates have been greater than that of U.S. T-Bills since later November 2023. These rates are most comparable with offchain T-Bill rates, as they are dollar-based and require no additional exposure to cryptocurrencies beyond stablecoins. The chart below tracks the supply rates of USDT, USDC, DAI and FRAX on Ethereum Mainnet.

Other News

Bitcoin surpasses silver to become second largest ETF commodity in the US

BlackRock's Bitcoin ETF hits $1B AUM in one week

Gitcoin-backed Layer 2 network PGN is winding down

Donald Trump says he’ll ‘never allow’ CBDC issuance if elected

Bitcoin mining hashrate falls by an estimated 25% amid Texas curtailment during major Winter storm

IRS says businesses don't have to report certain crypto transactions until new regulations issued

Chainlink integrates with Circle’s CCTP protocol for cross-chain USDC transfers

NFT wash trading volumes on Ethereum marketplaces hit lowest level in more than a year

Solana reveals Saga 'Chapter 2' Phone

Legal Disclosure:

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsementof any of the digital assets or companies mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2023. All rights reserved.